With the increasing prominence of responsible investment (RI) in the news, it’s more important than ever to know what investors really think about key issues. To cut through the fog and get a comprehensive understanding of the RI landscape in Canada, the 2023 RIA Investor Opinion Survey polled 1,001 individual investors for their opinions on AI, greenwashing, how they perceive RI and insights into their relationships with their financial advisors.

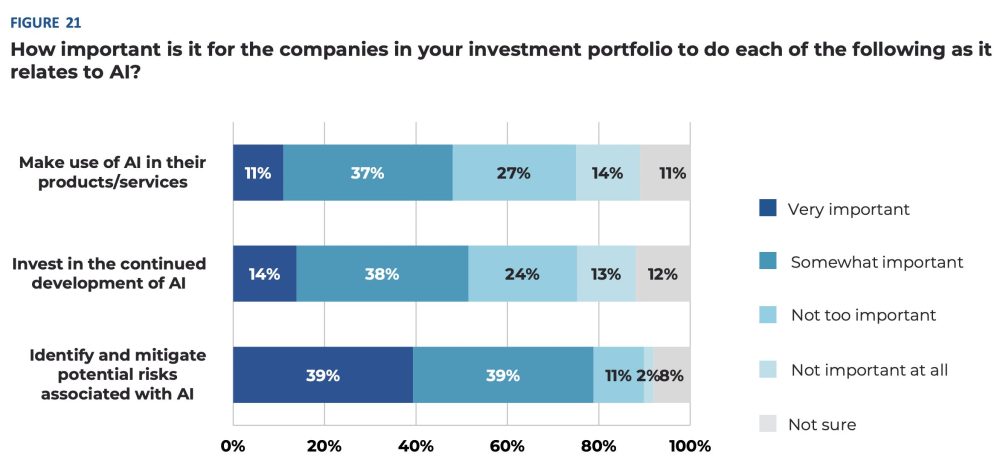

Investors view AI as more of a risk than opportunity

Nearly half of respondents (46%) view AI as much or somewhat more of a risk than an opportunity in terms of making responsible investment decisions. 8 in 10 said it is important for companies in their portfolio to identify and mitigate potential risks associated with AI, while half say it is as important for them to invest in the development of AI and make use of it in their products or services.

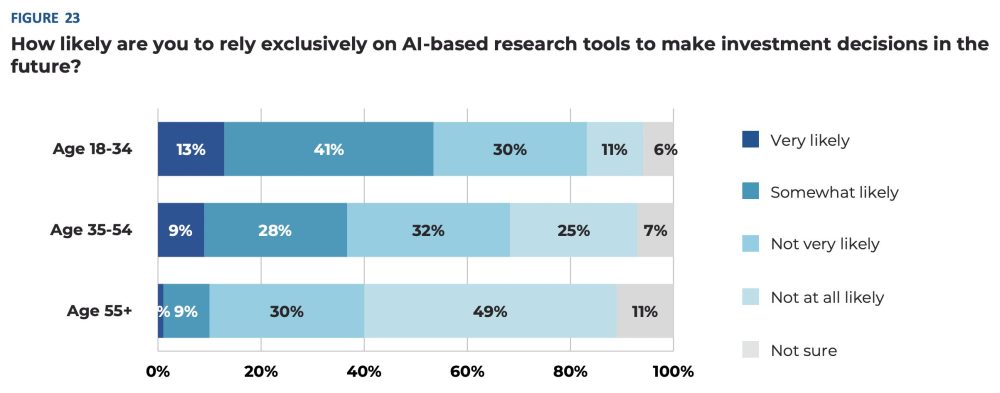

The majority of respondents (60%) say they are either not very or not at all likely to rely exclusively on AI-based research tools to make investment decisions in the future, with older respondents far more wary than younger ones.

Greenwashing concerns shrink, but remain prominent

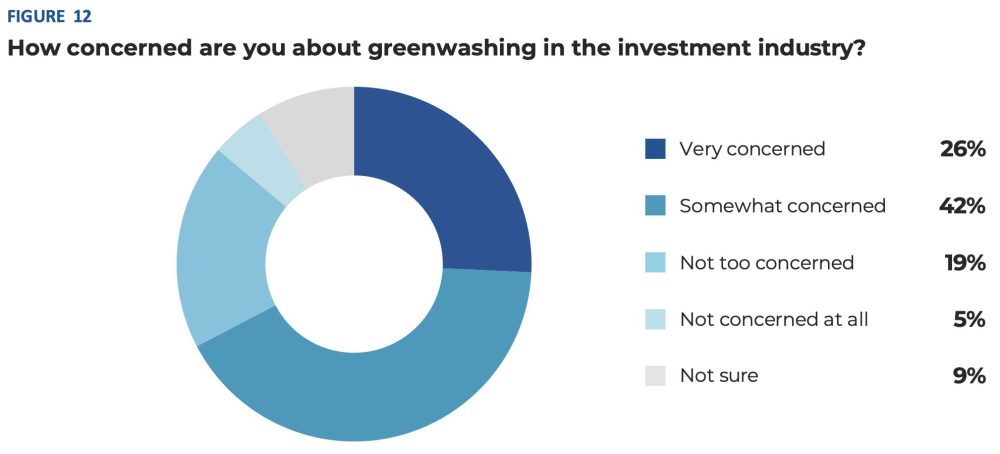

When asked about their level of concern with greenwashing in the investment industry, 68% of respondents say they are concerned. While this represents a strong majority, it shows a slight drop since 2022 (75%) and 2021 (78%).

Investment fund managers were initially provided with guidance from the Canadian Securities Administrators (CSA) on disclosures related to ESG considerations in January 2022, with a significant update in March 2024. There has been a notable increase in confidence among the majority of institutional investors and financial intermediaries in the overall quality of ESG reporting compared to a year ago. The greater focus on clarifying disclosure requirements and provision of reliable data in recent years and increased confidence in reporting may be helping to lessen concern about greenwashing among investors.

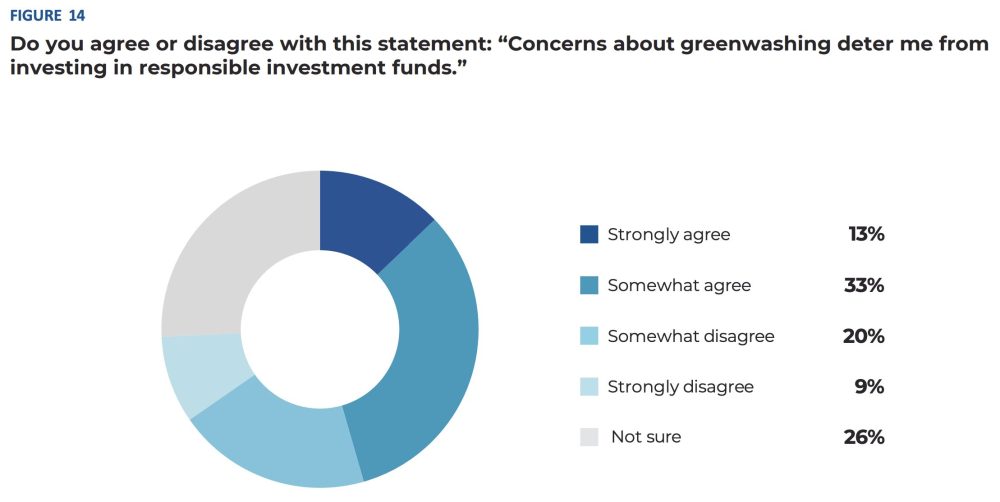

Despite this, greenwashing remains a prominent deterrent to the growth of RI. Nearly half of investors (46%) said greenwashing deters them from investing in RI funds with younger investors expressing the highest levels of concern. Similarly, the vast majority of financial advisors are highly concerned about greenwashing as it relates to RI, and concerns about lack of standards.

In Canada, there are ongoing efforts by regulators and industry to reduce the potential for greenwashing, particularly as it relates to investment fund disclosures for retail investors. In July 2022, the Canadian Investment Funds Standard Committee (CIFSC) published a Responsible Investment (RI) Identification Framework with the aim to provide clarity for investors who wish to invest in retail investment products (mutual funds and ETFs) with responsible investment strategies. And in February 2024, the CIFSC proposed changes to the Identification Framework to modify the existing definitions to align more closely with the terminology used in the global publication of Definitions for Responsible Investment Approaches (jointly written by the CFA Institute, Global Sustainable Investment Alliance, and the United Nations Principles for Responsible Investment).

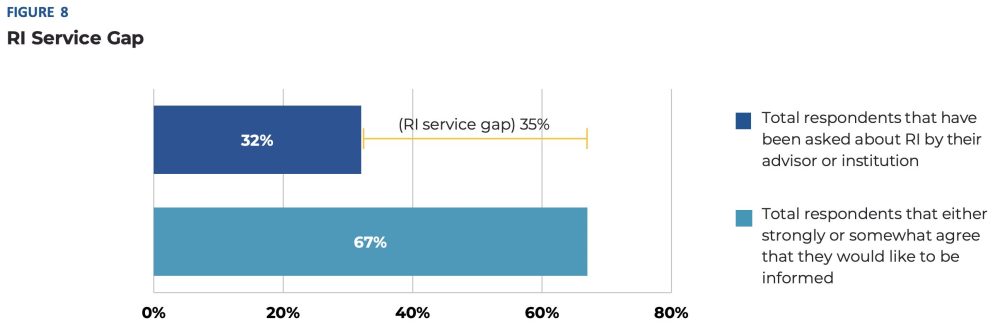

Closing the “RI service gap” remains an opportunity for RI Advisors

A strong majority of respondents (68%) either strongly or somewhat agree that RI can have a real impact on the economy and contribute to positive change for society, and 67% of Canadian retail investors want their financial services provider to inform them about RI. However, only one-third of their advisors have ever brought it up, meaning that one-third of investors are interested in RI, but not receiving the services they want.

This “RI service gap” presents a notable business opportunity for financial advisors who can engage clients on ESG topics and RI strategies.

Build your RI knowledge on May 28-29 in Vancouver at Canada’s leading RI conference. Join hundreds of advisors and investment professionals for an unparalleled two days of cutting-edge programming designed specifically for Canadian responsible investment professionals and advisors of all levels.

When we take the time to truly look at our world, it is hard not to be in awe of the expansive landscapes, majestic creatures, and delicate plant life.

Biodiversity describes the wide variety of life on our planet, spanning genetics, species, and ecosystems; more simply, plants, animals, and their surrounding habitats. Everything from the smallest flower to the largest blue whale reflects a piece of an intricate puzzle, which moves in an elaborate cycle to provide the fresh air, clean water, and natural resources that we collectively rely on to survive.

Beyond its beauty, biodiversity drives an underappreciated degree of our global economy in the form of natural capital. But it is increasingly at risk from climate change, chronic natural disasters, and human activity. This article highlights how the bond market has embraced biodiversity and how your portfolio can help protect our planet.

The economics of biodiversity

The World Economic Forum estimates that over half of the world’s GDP depends on biodiversity and the resulting natural capital which supports economic activity.

When the global ecosystem is thrown out of balance, it can have a dramatic ripple effect across economic productivity. For example, highly nature- dependent industries, such as agriculture and forestry, are threatened by land degradation, declining crop yields, and a rise in diseases and fungi that threaten plant life and core food sources.

Despite the economic and environmental importance of biodiversity, ecosystem loss is critical and growing. Land degradation threatens old growth forests, and an estimated one million species face extinction. Both acute climate disasters and chronic climate change continue to ravage some of the world’s most vulnerable and ecologically significant regions.

Further, as extreme weather events become increasingly frequent and severe, flooding, wildfires and power shortages threaten our way of life around the world. Destruction of the natural world poses a risk to global supply chains. The consequences include continuously elevated inflation and a climate refugee crisis.

Blended finance

The world of finance has long been defined by two measures to assess performance: risk and return. While each of these metrics may benefit from ESG integration, the most unique shift comes from addressing a third, potentially uncorrelated pillar: impact.

Blended finance is a concept that aims to have a positive impact by using development funding to leverage additional investment towards developing nations. Biodiversity and ecological stewardship can be a key to improving local economies by creating jobs and realizing the value of natural capital.

For governments and development banks, these opportunities have inspired some of the world’s most innovative transactions to source and mobilize investment in the most pristine and naturally significant ecosystems. Here are a few examples:

Wildlife Conservation Bond (Rhino Bond):

Threats to global biodiversity are perhaps most clearly seen through the increasing number of species that are now endangered. Deforestation, poaching, and habitat encroachment leave countless species at risk of extinction, from tiny bumblebee bats to the tallest giraffes.

In early 2022, the bond market saw the introduction of the first ever Wildlife Conservation Bond, a unique structure which links investor returns to positive outcomes. The aptly named “Rhino Bond” funds sustainable initiatives while investors forego their coupon payments, which are instead used to fund wildlife sanctuaries in South Africa.

At maturity, the World Bank and partner agencies will reward investors for their investment with a unique conservation success payment, linked to the growth rate of the black rhino population. By aligning the interests of investors, issuers, agencies — and rhinos — the bond market entered the biodiversity space like never before.

With 7.3% population growth in the first year, the Rhino Bond looks to double its ecological impact targets while delivering up to 50 basis points in premium yield over the life of the bond.

Debt-for-nature swaps:

While revolutionary, the Wildlife Conservation Bond structure is limited by its costly requirement for incremental financing from project sponsors including the Global Environment Facility. As central banks raised the cost of capital, the sustainable finance market experienced contraction alongside other debt issuers.

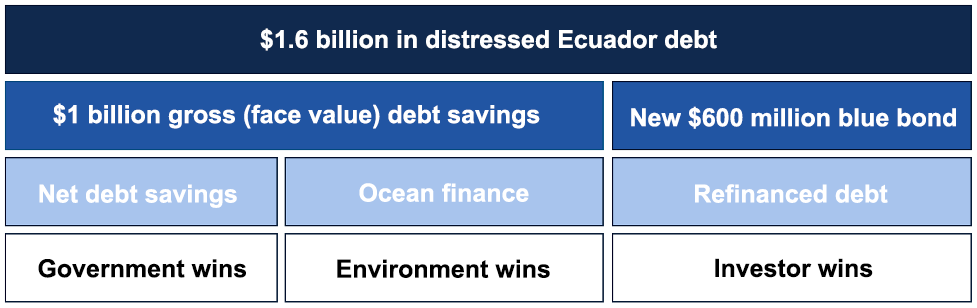

In May 2023, Ecuador completed the landmark “Galapagos Bond”, launching the world’s largest debt-for-nature swap in one of the world’s most biodiverse regions. In this transaction, Ecuador exchanged old bonds trading at distressed levels for new bonds in support of environmental protection.

This deal was made possible by Ecuador’s partnership with the Inter-American Development Bank and US International Development Finance Corp. The bond is expected to double the annual conservation funding efforts within the region, while committing to improved sustainable fishing regulations and reporting on the nationally protected Hermandad Marine Reserve. This region represents a key habitat for critically endangered species, as well as oceanic migration, and the bond’s innovative structure provides protection in line with the Global Ocean Alliance’s “30 by 30” pledge to protect 30% of marine territory by 2030.

In a unique transaction, Ecuador’s debt-for-nature swap provided support for investors, issuers, and the environment. Centred around the Galapagos Islands, this transaction is expected to generate $450 million in incremental financing towards marine conservation.

Investing in a better future

As investors, we often find ourselves looking past the short-term swings to focus on the future. Just as we hope our decisions will successfully help investors fund education, home ownership and retirement, we also aim to align our investments with a more sustainable world we hope to create.

We believe that our sustainable fixed income opportunities are also sound financial choices. When faced with opportunities to do good, while doing well, investing in sustainable fixed income solutions balances the needs of the present with the opportunities of the future.

Contributor Disclaimer

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of January 16, 2024. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. The content of this [type of marketing communication] (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

There has never been anything like it before. 2024 is the year the first companies within scope will be legally accountable under the European Union’s (EU’s) Corporate Sustainability Reporting Directive (CSRD). First reports are due in 2025 (based on fiscal year 2024 information). It is estimated that it will eventually also affect 1,300 Canadian companies directly, based on their business in the EU or listings on EU exchanges.

The CSRD is a European directive that marks a significant shift in the regulatory reporting environment as it sets out the rules for legally mandated accountability across a business’ entire value chain under the new and more robust European Sustainability Reporting Standards (ESRS). It is a reporting directive against the ESRS that embeds accountability for public and private companies to disclose actions taken to manage impacts on people and planet from business activities, and how the company is managing financially material ESG issues. The CSRD marks the beginning of a broader, sustainability regime designed to spur more proactive efforts and accountability to respect human rights and reduce carbon emissions and other environmental impacts linked to business activities. The Corporate Sustainability Due Diligence Directive (CSDDD or CS3D) is anticipated to follow once approved by European Parliament in April 2024. While the CSRD requires mandatory reporting against the ESRS, the CSDDD is a behavioural directive requiring companies to take action to prevent, mitigate, and remediate the most severe and likely adverse impacts from their business activities on people and planet. To ensure its passage following last minute erosion of support by multiple EU member states, changes to the CSDDD were negotiated in February and March 2024 to reduce its scope and scale so as to lessen direct impacts on small and medium-sized businesses. However it will still provide a legal liability mechanism for the largest companies operating in the EU to take responsibility for adverse impacts from business activities on society and the environment. In sum, this new sustainability regime is a gamechanger and has implications for entities even outside the EU. Below are high level answers to the following questions:

– What makes the ESRS unique? – How will they affect Canadian companies? – Why and how should Canadian investors encourage portfolio company alignment?

Key ESRS Features

Double Materiality approach

Entities must report their most significant impacts on people and planet (impact materiality) as well as sustainability risks and opportunities (financial materiality). Based on the United Nations Guiding Principles for Business and Human Rights (UNGPs) and the OECD Guidelines for Responsible Business Conduct.

Materiality Assessment

The ESRS starting point whereby companies must first detect and understand the most significant actual or potential impacts on people and planet across the entire value chain while also factoring in material risks and opportunities not related to the company’s outward impacts.

Scope

Applies to a company’s entire value chain (upstream supply chain, operations, and downstream customers) and requires enhanced reporting on both qualitative and quantitative information over short, medium, and long-term horizons.

Due diligence

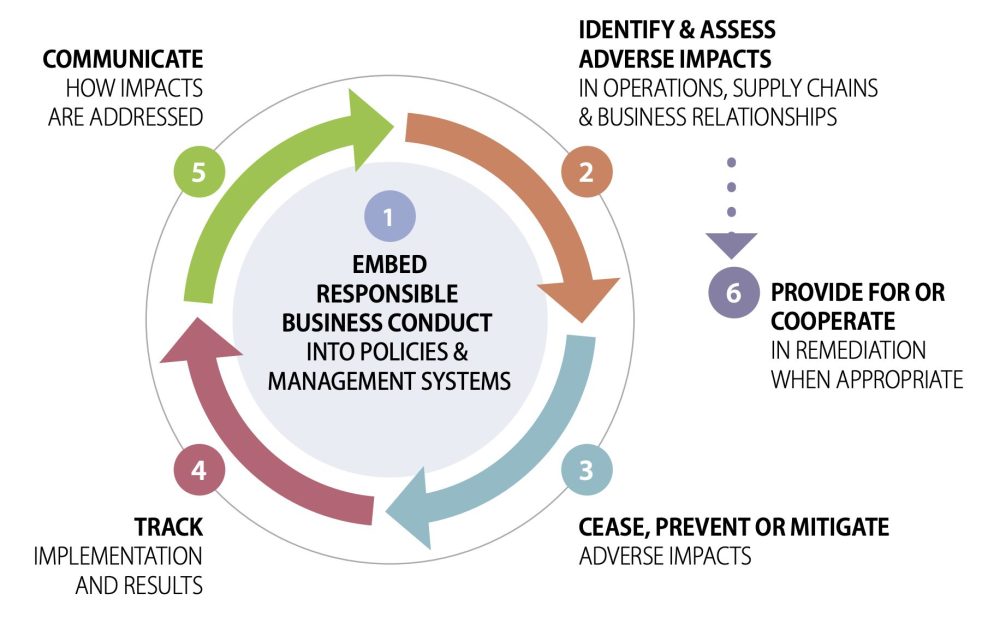

Mandates disclosure of practices to identify, prevent, mitigate, and account for the actual and potential most adverse impacts on people and the environment. This includes disclosure on how the views and perspectives of stakeholders and rights holders are ascertained and considered by senior management with respect to business model and strategy.

Assurance

Annual disclosures will initially require limited assurance by an accredited third-party auditor, expanding to reasonable assurance at a later date.

ESRS key features

A double materiality approach is the defining feature of the ESRS and provides the criteria to determine whether a sustainability topic or information has to be disclosed in reporting. Impact materiality refers to an entity’s material actual or potential, positive, or negative impacts on people and the environment while financial materiality refers to whether a sustainability topic generates risks or opportunities that impact an entity’s financial performance or position. Under ESRS, double materiality is the union of both these concepts. Adverse impacts on people and planet may not immediately pose a risk to a company’s bottom line but can become financially material over time.

The ESRS require companies to disclose methods and results of a materiality assessment of the entire value chain to ensure detection of the most significant (positive or negative) impacts from business activities for prioritization in management regardless of near-term financial materiality. This mirrors the fundamental first step in a do no harm, human rights due diligence process aligned with the OECDGuidelines for Multinationalsand the United Nations Guiding Principles on Business and Human Rights (UNGPs). Created in 1976 and 2011, respectively, these frameworks were developed and updated over the years to promote respect by businesses for international human rights laws, like the International Bill of Human Rights, which to varying degrees have been adopted into country laws around the world to hold states accountable to respect human rights. The CSRD, CSDDD and the ESRS now represent a new layer of accountability in that they legally enforce expectations for businesses to be accountable for respecting international human rights norms. This is by design. There are a considerable number of companies around the world already voluntarily committed to implementing the UNGPs and OECD Guidelines. Once transposed into the respective EU Members’ respective national laws, the CSRD and CSDDD will reinforce, and mainstream through hard law, already established, but voluntary, international human rights standards and frameworks to promote responsible business conduct.

Source: (OECD, 2018).

How does this compare with other large sustainability reporting frameworks? The ESRS seek additional comparability and consistency for topical disclosures through alignment to the greatest extent possible with other international topical standards developed by the Taskforce on Climate-related Financial Disclosures (TCFD), the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI). It should be noted, however, that the ESRS go extensively further than these frameworks because of the double materiality requirement.

The ESRS 12 topical standards are captured under four pillars as displayed in Figure 1. Note that social topical standards are broken down by stakeholder categories centring the need for careful consideration and prioritization of material impacts on these respective groups. Topical standards assessed by the company determined not to be material can be omitted. For each material topic, disclosure is required on:

–Business model and strategy. This includes reporting of baselines and time-bound targets, progress made toward targets, related company policies, actions taken to identify, monitor, prevent, mitigate, and remediate any actual or potential adverse impacts related to the matters in question, the result of these actions, and any relevant metrics. –Governance. This includes disclosure of diversity and skills to manage material sustainability matters at senior levels, how oversight is operationalized, whether there are dedicated controls and procedures applied to the management of impacts, risks and opportunities, how these are integrated with other internal functions, and how all of the above are factored into executive compensation.

General standards

Environmental standards

Social standards

Governance standards

1 – General requirements 2 – General disclosures

E1 – Climate change E2 – Pollution E3 – Water and marine resources E4 – Biodiversity and ecosystems E5 – Resource use and circular economy

S1 – Own workforce S2 – Workers in the value chain S3 – Affected communities S4 – Consumers and end users

G1 – Business conduct

Figure 1: ESRS topical standards

How will they affect Canadian companies?

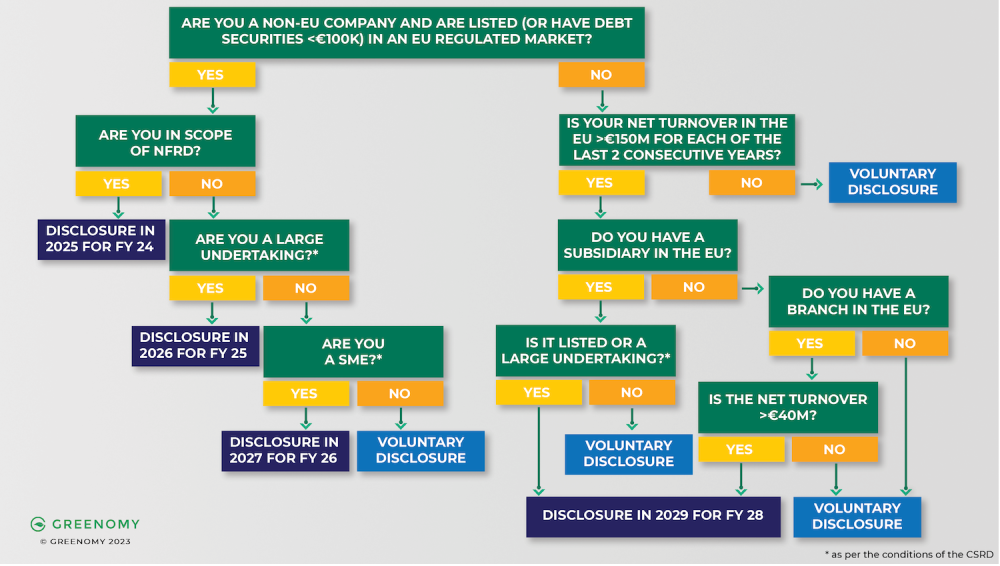

While the CSDDD will take longer to implement, the CSRD has already been enacted. Unlike the CSDDD, its scope provisions are wide, however, reporting obligations will be gradually implemented over the next five years (see Figure 2 below). It is anticipated it will eventually affect approximately 50,000 EU based companies, and around 10,400 foreign based companies directly, of which roughly 3,000 are American, 1,100 are British and 1,300 are Canadian. Indirectly, it will affect many more. Even if businesses do not have direct obligations under the CSRD they may still be asked for related disclosure by EU-based corporate customers, suppliers, lenders, and investors because the ESRS require companies within scope to report on human rights due diligence practices for their entire value chain.

Figure 2 provides a snapshot of the gradual implementation of CSRD obligations for non-EU based companies. Large Canadian entities who already report under the Non-Financial Reporting Directive (NFRD) and are listed on an EU regulated market will be required to disclose in 2025. Resources to help you understand which and when non-EU companies will be accountable under the CSRD can be found here.

Companies that have already implemented voluntary practices that align with the UNGPs and or OECD Guidelines will have an advantage with respect to ESRS. They will have processes in place to detect and understand their most significant, and therefore material, impacts as well as their obligation to prevent, mitigate, and remediate adverse impacts from business activities in addition to status quo financially material issues.

Already, some Canadian companies that are not directly within scope of the CSRD have begun implementing such practices to varying degrees. For example, certain Canadian miners with a large global footprint and as suppliers of the raw materials used in the manufacturing of a wide array of essential goods around the world, including by customers in Europe, are getting ahead of regulation by developing public policy and implementing practices aligned with the UNGPs. This sector in Canada appears to be leading in its understanding of the long-term implications of Europe’s new and robust sustainability regulation on future growth prospects and subsequently, for business practices. But there is still a lot of work to be done to ensure accountability. Investors can play a role.

Figure 2: CSRD reporting for non-EU companies: What you need to know. Note: Net turnover threshold was increased from €40 to €50 million. Non-EU parent companies of EU listed or based subsidiaries must provide consolidated ESRS aligned disclosures.

CSRD non-EU scope requirements will evolve over 4 years

Disclosure due in 2025 for FY 2024: Large non-EU companies (more than 500 employees) with securities listed on an EU-regulated market (with the exception of micro-enterprises).

Disclosures due in 2026 for FY 2025: Large* non-EU companies listed on an EU-regulated market.

Disclosures due 2027 for FY 2026: Certain non-EU small and medium sized enterprises (“SMEs”) listed on a regulated market in the EU.

Disclosure due in 2029 for FY 2028: Non-EU companies that have net turnover in the EU > € 150M for prior 2 consecutive years

Non-EU company that has a subsidiary in the EU that is either listed or considered a ‘large’ undertaking.

*Large as per CSRD is exceeding two of the following three metrics on two consecutive annual balance sheet dates:

– Total assets of €25M – Net revenue of €50M – Average 250 employees or greater

NOTE: Non-EU parent companies of EU listed or based subsidiaries must provide consolidated ESRS aligned sustainability reports. There are also a number of reporting exemptions for non-EU companies reporting under different regimes, however, these haven’t yet been finalized.

Why and how investors should encourage portfolio company alignment now

By May 31, 2024 a broad swathe of Canadian companies and institutions are required to report on their efforts to prevent and reduce their risk of using forced or child labour directly or in their supply chains, as per Canada’s newly enacted Fighting Against Forced Labour and Child Labour in Supply Chains Act. While this act is a mere drop in the bucket compared to the depth of Europe’s mandatory human rights and environmental due diligence accountability regime, companies can use it as a prime window of opportunity to ready and test their human rights-related policies, processes, and oversight mechanisms in case they need to report under CSRD or as part of a supplier or service provider of a company reporting to CSRD. Where to start? Voluntary commitment to and adoption of the UNGPs.

In early 2023 BMO Global Asset Management published a deep dive research report that found that Canadian companies are in early stages of readiness for alignment with the UNGPs. Canadian companies make decent voluntary policy commitments but can improve on implementing human rights due diligence. Given that the ESRS, which makes the UNGPs and human rights due diligence mandatory, is an indication of the future direction of travel of what will be considered the highest bar in a global marketplace, investors can help Canadian companies maintain their competitiveness.

Investors can encourage best practices through:

1) Education (if not already aware) on international human rights standards (such as the International Bill of Human Rights, UNDRIP, and others) and frameworks for human rights due diligence (UNGPs and OECD Guidelines). 2) Development of investor human rights policies that set clear expectations for alignment with international human rights standards and frameworks in investment decision making and investee company practices. 3) Development of systematic investor human rights due diligence procedures to implement policy commitments on human rights and ensure investors do not contribute to adverse impacts. 4) Engagement with investee companies on human rights policies and practices e.g., asking companies what their most significant positive and negative impacts on people and planet are throughout the value chain and what they are doing to prevent and mitigate negative impacts. 5) Communicate investor expectations to investee companies and use investor leverage to encourage adoption and implementation of practices that align with international human rights standards and frameworks that will simultaneously help future-proof companies against the EU’s new robust sustainability regime and any other similar regulations in other regions that may evolve over time.

Contributor Disclaimer

This communication is intended for informational purposes only and is not, and should not be construed as, investment, legal or tax advice to any individual. Particular investments and/or trading strategies should be evaluated relative to each individual’s circumstances. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Past performance does not guarantee future results.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent simplified prospectus.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

®/™Registered trademarks/trademark of Bank of Montreal, used under licence.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Companies offering multi-class shares with unequal voting rights have recently garnered renewed debate and interest from investors and market participants. In April 2023, the S&P Dow Jones Indices reopened certain indices to companies with multiple share classes under certain circumstances, a reversion from its 2017 decision to bar such companies from inclusion. Among Russell 3000 companies excluding the S&P 1500, there has also been an increased number of companies with unequal voting rights in recent years. “Between 2019 and 2022, the percentage of Russell 3000 companies excluding the S&P 1500 with unequal voting rights increased from 11.2% to 15.7%,” according to a report from Institutional Shareholder Services, a leading proxy advisory firm better known as ISS.

As of 2023, ISS and Glass Lewis, another leading proxy advisory firm, both have policies within their proxy voting guidelines which hold company directors accountable if a company employs a common stock structure with unequal voting rights in certain markets. While the market has swayed back and forth on the case for unequal voting rights, investors generally prefer following the one-share, one-vote principle.

Engagement as Independent Minority Shareholders in Controlled Companies with Unequal Voting Rights

There is an abundance of academic debate on ownership structures and shareholder returns, including arguments for and against the merits of founder- or family-controlled companies with unequal voting rights. However, there are certain challenges from an investor stewardship perspective for independent minority shareholders.

Issues of corporate governance, including minority shareholder rights, are often intertwined with environmental and social controversies, as many of these issues require the oversight afforded by good governance structures, which includes boards being able to respond effectively to shareholder concerns as represented by shareholder votes. Where votes are controlled disproportionately, most likely by founding executive officers who also wield significant and sometimes majority board influence through direct representation, companies might be less likely to respond to investor concerns on certain environmental or social issues. This is because the shareholder vote results, which invariably will be majority-supported and a reason used by some to legitimize the status quo, will not be reflective of independent shareholder voices when including control blocks. Even if such a company’s board is significantly independent (beyond majority), the prospect of the controlling shareholders’ votes being used to vote against and threaten an otherwise independent director’s election may discourage directors from expressing dissenting views.

This is one reason why unequal voting rights through multi-class shares are uniquely problematic: this setup could foster governance structures and boardrooms where the mandate of oversight gets lost to the certainty of success when it comes to voting outcomes. Investors who take issue with unequal voting rights among multi-class share structures have long advocated for their collapse or sunset, and some have begun to vote against the directors of such companies. However, if investee companies have not been responsive, and shareholder vote results are not very impactful given the controlled status of the vote, then it is equally important for investors to advocate for measures which ensure that independent shareholder voices are heard. This can occur by ensuring that boards have formal avenues for responding to independent shareholder concerns, irrespective of the capital structure of the company.

What Can Independent Minority Shareholders Do?

There are certain requests that minority shareholders can present to investee companies controlled via unequal voting rights in order to address the issue of inaction when it comes to problematic multi-class share structures. These actions are not meant to replace what other market participants have rightly been asking for. Rather, they serve to complement an investor’s existing actions on voting, engagement and advocacy.

An investor can ask investee companies how independent shareholder votes are considered at the board level, excluding the impact of controlling shares. Investors should know if the board is formally considering the impact of the independent shareholder votes in a timely manner. Investors should also understand if deliberations at the board level include discussions on how the company intends to respond to shareholder views expressed through their votes. A shareholder proposal receiving majority independent shareholder support or a director not receiving the requisite independent shareholder vote, despite receiving a majority of votes in support when including controlling voting blocks, should warrant and trigger the right discussions at the board level.

An investor can also ask investee companies to consider implementing and publicly disclosing formal policies, procedures or frameworks which outline how exactly the board intends to take independent shareholder votes into consideration. This should include how the board calculates and reviews vote results after an annual meeting and there should be clear directives outlining what happens as a result. Let’s say a company has a director elected via majority shareholder support inclusive of controlling shares but does not meet the requisite support levels when considering only independent shareholder votes. In that case, a hypothetical framework may be to assess the independent shareholder vote results at the board level, consider responsive actions within 90 days, if any, and/or disclose those details in the next year’s proxy statement.

These formal policies or procedures, which can be adopted and disclosed by company boards, will hold companies accountable to, at minimum, reviewing the independent shareholder votes. It will also allow investors to initiate conversations about the types of actions that have resulted from what companies said they would do versus what they have done. For shareholder proposals that made it to the vote, unless a substantially similar proposal is filed in the following year where companies choose to include such additional information about how their boards have been responsive in their company response statement, companies are not even obliged to disclose the outcome of any board deliberations, considerations or responsiveness actions. Therefore, the adoption of a formal policy or procedure and its disclosure could help companies standardize the ways in which they respond to shareholder concerns, relay information internally to the board and disclose relevant information to investors.

Contributor Disclaimer

The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

This document may contain forward-looking statements (“FLS”). FLS reflect current expectations and projections about future events and/or outcomes based on data currently available. Such expectations and projections may be incorrect in the future as events which were not anticipated or considered in their formulation may occur and lead to results that differ materially from those expressed or implied. FLS are not guarantees of future performance and reliance on FLS should be avoided.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

The shift from Indigenous participation to Indigenous leadership through active influence and Indigenous equity investment in major projects in Canada has accelerated in recent times. This shift has been at the behest of unrelenting Indigenous work and leadership, and more recently supported by capacity maturity, collaborative government supports, and increased capital market interest. However, the full benefit of Indigenous ownership and participation is being realized creating greater value not only for the Indigenous nations that are involved, but also for the projects and surrounding economy as a whole.

A New Era of Indigenous Participation

Indigenous nations are recognizing that the value of equity participation in project development isn’t only in the revenues generated, but in the opportunity to gain valuable experience in the development process, in operations, and in policy and decision-making roles. Through this greater depth of engagement, Indigenous asset owners are seeing a maturity of capacity and building strong commercial and industrial experience that positions Nations for increasing leadership in subsequent developments. Active equity participation operationalizes governance for Indigenous decision-making at board tables to materialize into on-the-ground activities that directly impact the Nation membership they represent. Leaving behind the bare-minimum standard of a few short-term jobs for the Indigenous nation today has emerged as Indigenous equity ownership as leaders and decision makers in prime contractor selection and contract administration, including Indigenous procurement at every level of the supply and value chains.

Government interest and support in Indigenous economic reconciliation has played a role in the advancement of Indigenous equity participation. In Canada, governments have increasingly upheld Indigenous rights and established standards for Indigenous leadership in environmental and cultural impact assessment. Concurrently, they have created pathways to accessing affordable capital through mechanisms such as loan guarantee programs. By doing so, they have set a predictable and effective landscape for Indigenous nations active investment in project development. Innovations such as the loan guarantee program, first deployed by Alberta Indigenous Opportunities Corporation, are being emulated in other provinces, with also commitments from the Federal Government. These programs are what facilitate access to affordable, non-recourse financing solutions, which ultimately support Indigenous nations equity participation.

Unlocking True Value Through Indigenous Equity Projects

Capital markets, buoyed in confidence by the supports assured by governments in the form of Indigenous loan guarantee programs and other credit enhancements, have sat up and taken notice this shift in Canada. As industry’s literacy around Indigenous partnership grows, the competitive landscape is becoming one where the market’s keen interest is illustrated in the reducing costs of capital. Indigenous equity ownership in major projects are increasingly seen as not just ‘one way’ or ‘a good way,’ but as the ‘best-‘ or ‘only way’ to develop energy, net zero, infrastructural, or critical mineral projects in Canada. The confidence of capital markets translates through more competitive rates to higher profitability for Indigenous equity holders in those projects.

The full benefits that project equity can bring to Indigenous nations can only materialize when those Indigenous partners exercise their influence through active participation in project development. By not only being at the table, but having influence at all levels of decision-making, Indigenous equity holders can fortify developments with Indigenous values and fully realize the ripple effects of economic growth on the health and wealth of their Nation membership and beyond.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Last year was full of accomplishments for the RIA, from the success of our first in-person Conference since 2019, to our global and local industry research, and convening with members in major cities across Canada. None of this would have been possible without the commitment and engagement of our members, which is why we conducted a comprehensive Member Survey to inform our strategic direction and set us up for an extraordinary 2024.

We’ve started the year with a focus on the RIA’s evolved strategy and plans to enhance our member experience. We will also be offering redesigned approaches to optimize online learning and look forward to increasing our voice in policy and advocacy work.

On February 26th, we will be in Montreal hosting an afternoon of French language discussions on economic reconciliation and responsible investment, followed by an evening cocktail reception. Later that week we will launch the 2023 RIA Investor Opinion Survey, examining Canadian investors’ attitudes toward responsible investing. This will be the RIA’s eighth annual survey of individual investors and it is based on data from over 1000 respondents across Canada. A presentation of the results will be available in both French and English.

In May, we will convene for the first RIA Conference in Vancouver since 2017 and are excited to meet members from across the country. The conference serves both institutional and retail markets, offering opportunities to network with industry leaders, hear from ESG specialists, and learn about the latest issues, trends and developments in the field. Previous RIA event speakers include industry change-makers, visionaries, policy makers, sustainability leaders, and practitioners, and we are excited to share this year’s lineup in the coming weeks.

Moving into the fall, we will welcome the global sustainable investment community for PRI In Person in Toronto, and look forward to hosting our Global Sustainable Investment Alliance (GSIA) colleagues in person. We will also deliver the third consecutive annual RI Trends Report, an important milestone in tracking the evolution and maturity of our industry.

We look forward to engaging with you and sharing exciting developments as the year progresses.

There will be no global net zero unless the energy transition in emerging markets is accelerated rapidly. That requires urgent action by the financial community.

Among developing nations, which now account for more than half of total emissions and rising, China alone has available resources to fund its energy transition. The rest of the developing world requires a massive increase in overseas investment. According to the International Energy Agency, roughly US$1 trillion of annual funding is required to decarbonize emerging economies (not including China). As of 2021, less than one-sixth of that sum was being spent.

Less than 1% of the institutional asset pool would be required to meet all of the developing world’s net zero financing needs. The problem is not a shortage of capital per se. Global institutional assets, most of which are managed by pension and sovereign-wealth funds, add up to about US$120 trillion.

Many allocators we speak to understand the ‘why’ but ask how assets can be mobilized to support the energy transition in emerging markets, while also contributing to their return targets. The first step is for asset owners to recognize that in order to meaningfully contribute to the lowering of global emissions, they must shift their allocations – and hence their influence – toward high-emitting companies, industries, and countries. This means allocating to the developing world especially. To date, too many have sought to clean up their portfolios by doing the opposite.

13 of the 20 biggest carbon emitters are emerging economies. Large emitters among them include a diverse group classified by the OECD as middle-income countries, such as Brazil, China, Colombia, India, South Africa, Thailand, and Turkey. Together, they account for 56% of the greenhouse gases put into the atmosphere each year. Ex-China, they still represent about one-quarter of global emissions. Most of them have fairly sophisticated private sectors and financial systems, offering broad opportunities and multiple access points for international capital.

The second step, and perhaps the most important, is to dispel the myth that transition investing in emerging markets is a charitable undertaking. The ‘emerging transition’ investment universe is large and robust enough – and, crucially, generating sufficient economic value within individual nations – that it offers commercial returns. By sector, most of the transition investment in emerging countries needs to be directed toward building out renewable-energy generation capacity and upgrading the electricity grid. In our view, these and other transition-linked areas of emerging economies can be extremely competitive from a risk-return perspective.

The third step is for pension funds and other large asset owners in advanced economies to become more familiar with the most effective channels for transition investing in emerging markets: corporate debt and project financing. While many developed-world pension funds currently have an allocation to emerging markets via equities and sovereign debt, very few invest in emerging credit. Yet this is a deep market, offering a highly efficient pathway to connect institutional asset pools with the businesses and projects at the heart of the emerging world’s energy transition. Moreover, by advancing climate-oriented covenants and embedding meaningful carrots and sticks in bond and loan documentation, investors can incentivize progress toward net zero in a targeted and effective way.

Ninety One’s emerging markets corporate debt team alone manages investments in more than 40 countries – there are many private- and public-sector entities with serious net-zero intent seeking transition financing. The latter are often running well ahead of the former. In India, for example, whose national climate targets are generally seen as lagging, almost 100 companies have now adopted science-based emissions-reduction targets. In South Africa, Anglo American plans to install up to 4GW of renewable-energy capacity by 2040, which could see the mining giant generate about 7% of its home nation’s electricity needs. In short, the building blocks exist to accelerate the emerging world’s energy transition: the capital, via institutional asset pools; the ambition, not least via emerging market companies’ transition plans; and the mechanisms, of which the credit markets are arguably the most important. The urgent task now is to connect and action them.

Contributor Disclaimer

This communication is for professional investors and financial advisors only.

The information may discuss general market activity or industry trends and is not intended to be relied upon as a forecast, research or investment advice. The economic and market views presented herein reflect Ninety One’s judgement as at the date shown and are subject to change without notice. There is no guarantee that views and opinions expressed will be correct and may not reflect those of Ninety One as a whole, different views may be expressed based on different investment objectives. Although we believe any information obtained from external sources to be reliable, we have not independently verified it, and we cannot guarantee its accuracy or completeness (ESG-related data is still at an early stage with considerable variation in estimates and disclosure across companies. Double counting is inherent in all aggregate carbon data). Ninety One’s internal data may not be audited. Ninety One does not provide legal or tax advice. Prospective investors should consult their tax advisors before making tax-related investment decisions.

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Since OpenAI’s ChatGPT went viral in late 2022 for its unprecedented ability to engage in human-like conversations and provide articulate responses in wide-ranging domains of knowledge, several competitors have begun introducing their own iterations of the technology. This type of AI technology, known as generative AI, is based on large language models that are trained on massive amounts of data, which could include text, images or other media. The models identify the patterns and structures of the training data and then generate new content that has similar characteristics based on user prompts.

There are various benefits to incorporating generative AI in a business – process improvements, cost reduction and value creation, to name a few. Leveraging these opportunities, companies across different sectors have already begun testing and implementing generative AI tools. Examples range from financial institutions deploying chatbots trained on internal databases to provide financial advice to customers, to healthcare institutions automating the generation of medical documentation based on conversations between patients and physicians. Across industries, companies are also incorporating generative AI tools in marketing, customer service and product development.

As such, investors have to pay attention not only to large tech companies that are building the foundational models, but also to companies that are starting to incorporate generative AI tools into their business. As with most new technologies, there are potential risks that should be adequately considered and safeguarded against before widespread deployment. Regulation will be important in helping reduce these risks. But because the development of regulation occurs at a much slower pace than the development and application of AI, investors should actively consider its risks and seek stewardship opportunities in companies involved in generative AI to address these risks.

Challenges and Risks in Generative AI

Generative AI models have various known issues. These models have the tendency to “hallucinate,” generating false outputs that are not justified by the training data and presenting them as a fact. These errors can be caused by various factors, such as improper model architecture or noise and divergences in the training data. Opaqueness about the generation of model outcomes is also an issue. With billions to trillions of model parameters that determine the probabilities of each part of its response, it is exceedingly difficult to map model outputs to the source data, including in cases of hallucination.

In addition, if the training data contains societal prejudices or if the algorithm design is influenced by human biases, the model may learn and propagate these biases in its outputs. Enterprise applications could also be vulnerable to data privacy issues and cybersecurity threats. This includes leakage of sensitive information within the training data if the model is customer/public-facing, usage of personal or sensitive data in model training that may have needed explicit consent to use, as well as malicious attacks from hackers that aim to manipulate model outputs.

These issues give rise to various legal and reputational risks, the scale of which depends on the criticality of the use case and the company’s industry. For example, the financial and healthcare industries may be subject to severe consequences if problems do arise, due to the high-stakes nature of these industries.

Sample Use Cases in the Financial Industry

In financial advisory use cases, model hallucinations could give inappropriate advice or offer the wrong product to undiscerning clients, which could undermine public trust in AI systems and the financial institutions using them. Lack of transparency about the generation of model outcomes is also a key issue for financial institutions, as these institutions are required to be able to explain their decisions internally and to external stakeholders. Considering all this, it is best practice to implement a degree of separation between direct model outputs and the customer, where internal staff could be trained to recognize potential errors and inconsistencies in model outputs and assume ultimate responsibility for the decision-making process.

Generative AI could also offer a quick and low-cost way for financial institutions to profile their clients for marketing campaigns, risk management and identification of suspicious transactions. However, overreliance on generative AI profiling could violate anti-discrimination laws due to potential bias embedded within the models. Appropriate human judgment will need to complement generative AI models that perform client profiling. Financial institutions will also need to have strong data privacy policies and robust cybersecurity measures to address generative AI’s risks to their sensitive client information and proprietary data.

Questions for Investors to Consider

In view of all these issues and risks, below are questions investors should consider when assessing companies employing generative AI tools:

What are the risk-mitigating mechanisms and/or circumstances? Solutions include having trained internal staff act as an intermediary between direct model outputs and the customer; working to understand potential biases in the training data and address them in model design; regular and proactive monitoring of model output to promptly identify and address any signs of hallucinations; implementing robust cybersecurity measures; etc.

What is being done to enhance model performance? Solutions include ensuring that training data is of high quality, accurate and up to date; implementing iterative feedback loops to refine and improve model performance; etc.

Is there any transparency and oversight ofethical AI principles? This pertains to providing transparency on data sourcing and data privacy concerns; defining clear policies and procedures to ensure compliance with ethical standards and emerging regulations; outlining the roles and responsibilities of individuals involved in the development, operation and oversight of the generative AI model; etc.

Contributor Disclaimer

The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. The information does not provide financial, legal, tax or investment advice. Particular investment, tax or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

This document may contain forward-looking statements (“FLS”). FLS reflect current expectations and projections about future events and/or outcomes based on data currently available. Such expectations and projections may be incorrect in the future as events which were not anticipated or considered in their formulation may occur and lead to results that differ materially from those expressed or implied. FLS are not guarantees of future performance and reliance on FLS should be avoided.

The statements and opinions contained herein are those of Kate Tong and do not necessarily reflect the opinions of, and are not specifically endorsed by, TD Asset Management Inc.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Nuclear power has been a somewhat neglected energy source for some years now. It provides only around 10% of the world’s electricity (and around 15% of Canada’s), and currently comes far behind oil and natural gas in terms of overall global energy supply.

However, there are big changes coming in how the world will consume energy. To mitigate the impacts of global warming, most countries have made significant commitments to move away from fossil-fuel use and replace it with net-zero energy. To achieve this within the fairly short timeframes required (2050 for many countries), nuclear power is likely to become a much bigger player in the electricity-generating field.

Let’s take a look at the scope of change as the world moves from fossil fuels to net-zero energy sources; nuclear power’s probable role; and the investment opportunities that it brings.

Net-zero targets and the move away from fossil fuels

Extreme weather, exacerbated by global warming, has had devastating impacts on the planet, causing billions of dollars’ worth of damage along the way. In a bid to minimize these impacts, most of the world’s countries have agreed to cut human-made greenhouse gas emissions to restrict global warming to no more than 1.5 degrees Celsius above pre-industrial levels. The world is currently around 1.1 degrees Celsius warmer than it was in the late 1800s.

According to the Paris Agreement (a legally binding international treaty on climate change), greenhouse gas emissions need to be reduced by 45% by 2030 and reach net zero by 2050. To achieve this, we’ll need to make a huge shift regarding the type of energy we use in every aspect of our lives: for light, heat, cooling, transportation and industry. The world will gradually have less dependency on fossil fuel energy — such as coal, gas and oil — and replace it with renewable energy sources.

This will be a mammoth task, and while it won’t happen overnight, it does need to happen in just a few decades, which will bring with it considerable challenges.

Nuclear power’s role in reaching net-zero targets

Currently, with almost 85% of global energy consumption coming from fossil fuels, we clearly have a long way to go to greatly reduce that consumption and diversify the energy grid.

The good news is that the journey has already begun, and renewable energy sources, such as hydro-electric, solar and wind power are not only growing at a fast pace, they’re also less expensive to set up when compared to new gas or coal generating plants.

Much of current fossil fuel energy will have to be replaced by electricity in one form or another (either directly from the power grid or in batteries). One of the key issues of renewable energy is storage. The technology to store excess energy from wind and solar farms when the sun is shining and the wind is blowing, is currently insufficient. When it’s dark and still outside, we’ll need an energy source that can continue to feed our power needs. While hydroelectric power (using the power of moving water to generate electricity) is highly efficient at providing energy at the push of a button, wind and solar are not.

This is where nuclear power comes in. While it’s not renewable energy as such (uranium, the source of nuclear power, is a finite resource), it does create energy with zero greenhouse gas emissions. And it can deliver energy around the clock, regardless of the weather or time of day.

There is substantial potential for increased growth of nuclear energy over the short term, to help replace the huge amounts of fossil fuel energy we currently consume. It can be a quick and fairly cost-efficient option to extend the life of nuclear reactors so they can continue to generate power. Also, the development of small modular reactors (SMRs) could provide a more affordable option that is much faster to build than large reactors.

In recent years, there seems to have been concerted political will for nuclear power to play a key role in the transition to net-zero emissions. In 2020, then Minister of Natural Resources, Seamus O’Regan said, “We have not seen a model where we can get to net-zero emissions by 2050 without nuclear.” Nuclear currently accounts for 15% of Canada’s electrical production capacity.

The challenges facing nuclear power

Nuclear power has some hurdles to overcome when it comes to being a key player in the move away from fossil fuels. Some of these issues are contentious, but they’re all worth mentioning, and include:

New nuclear power plants are expensive to build and take years to complete.

It’s perceived to be dangerous: disasters like those that happened in Fukushima in 2011 and Chernobyl in 1986 have given nuclear power a reputation for being unstable.

Uranium mining can have negative environmental impacts.

Nuclear power generation uses large amounts of water.

Radioactive waste from nuclear power stations can remain dangerous for thousands of years, and storing it safely can be a challenge.

The nuclear power industry has been working to overcome these challenges. For example, small modular reactors have the potential to produce energy quicker and cheaper than large power plants. And when compared to other means of power generation, nuclear is fairly safe, especially when you consider there have been two major disasters in 37 years among the world’s 440 nuclear power stations.

And, given nuclear power’s ability to produce large amounts of electricity efficiently and continuously, without being beholden to the weather or sunlight, along with political will, it looks set to play a key role in the transition away from fossil fuels.

Investment opportunities in nuclear power

Nuclear power’s main attraction for investors is that it’s a zero-emission energy source that can easily adjust its output to match demand, unlike the current challenges facing renewable energy sources such as wind and solar. As the world moves away from oil, gas and coal, huge amounts of carbon-free energy will be needed. Nuclear power is well positioned to help the world reach net-zero energy consumption.

Governments are committed to transitioning to zero-emission energy by the end of the century, and many are providing tax incentives for nuclear power generation. For example, Canada has a tax credit of up to 30% for clean energy technologies, which include small modular reactors, and the US introduced a tax credit in 2022 for the production of new nuclear power.

Here are some of the key ways that nuclear power can offer investment opportunities:

The development of small modular reactors could be extremely attractive. They can be built in a factory and then shipped to the site, meaning that they could be used to provide power to many remote or small communities.

Traditional nuclear power will only grow in importance as more countries upgrade existing (or build new) nuclear reactors to meet aggressive net-zero targets.

Many businesses are built around the maintenance and upgrading of traditional nuclear reactors, a sector that is likely to grow enormously over the next few decades.

To find out more about the role that nuclear power will play in the move away from fossil fuels, and the investment opportunities it will bring, read the Mackenzie Betterworld Team’s Pathway to net zero.

Contributor Disclaimer

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of November 8, 2023. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. The content of this [type of marketing communication] (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

In the rapidly evolving world of responsible investment (RI), it’s more important than ever for investment professionals to stay at the leading edge of what’s current and what’s around the corner in sustainable finance.

On October 26, the RIA will be officially launching the latest edition of our Canadian RI Trends report, the most comprehensive research survey and analysis of responsible investment assets and trends in Canada. Last year, the 2022 Report confirmed that RI’s recent momentum was giving way to demand for sophistication and more vigilant reporting, signaling a maturing industry. The 2023 Report will continue to track national trends and outlooks, as well as provide insights into the most common practices of responsible investors in Canada.

Advancing RI expertise among our members is a priority for the RIA. Our latest survey of over 1,000 retail investors shows that Canadians want to hear more about responsible investment. While nearly three quarter of respondents wanted their financial services provider to inform them about RI, only a third said their financial services provider had broached the subject with them. That leaves a significant business opportunity for those with an up-to-date understanding of RI.

To keep you on the cutting edge of RI this fall, we’ve brought together top experts, thought leaders and practitioners for four bi-weekly webinars covering:

– The results of the 2023 Canadian RI Trends Report – The ethical implications of AI and what they mean for investors – The opportunities of incorporating climate solutions into investment strategies – The critical connection between climate change adaptation and sound investment decisions

Don’t miss the 2023 RIA Fall Forum Series for the latest trends, topics, and what’s around the corner in responsible investment.