Governments around the world are committed to meeting their climate change objectives. The ability to achieve lower carbon emissions rests on a successful transition to renewable power and lowering emissions in transportation and manufacturing. The world will need a massive quantity of critical metals and securing the primary supply will be key. Meeting that demand will require significant capital, which we believe will create a multi-decade investment opportunity. Historically the mining industry has not been embraced by responsible investment approaches, however lowering carbon emissions cannot happen without the mining industry providing the crucial inputs. We believe there is the potential for a strong alignment between supporting the energy transition and earning strong investment returns.

Growth in Electric Vehicles

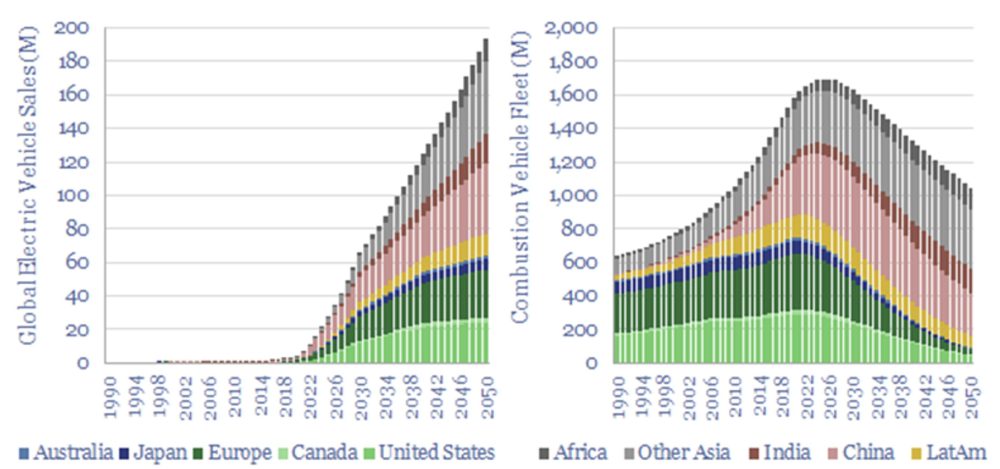

While there are many areas that are transitioning toward lower emissions, for this article we focus on electric vehicles (EVs) to illustrate the complexity and scale of the transition challenge for the mining industry. EV production and demand are growing rapidly. According to Thunder Said Energy, electric vehicles accounted for 12.5% of all new global vehicles in 2022, and is projected to be 50% in 2030, or 65 million units [1].

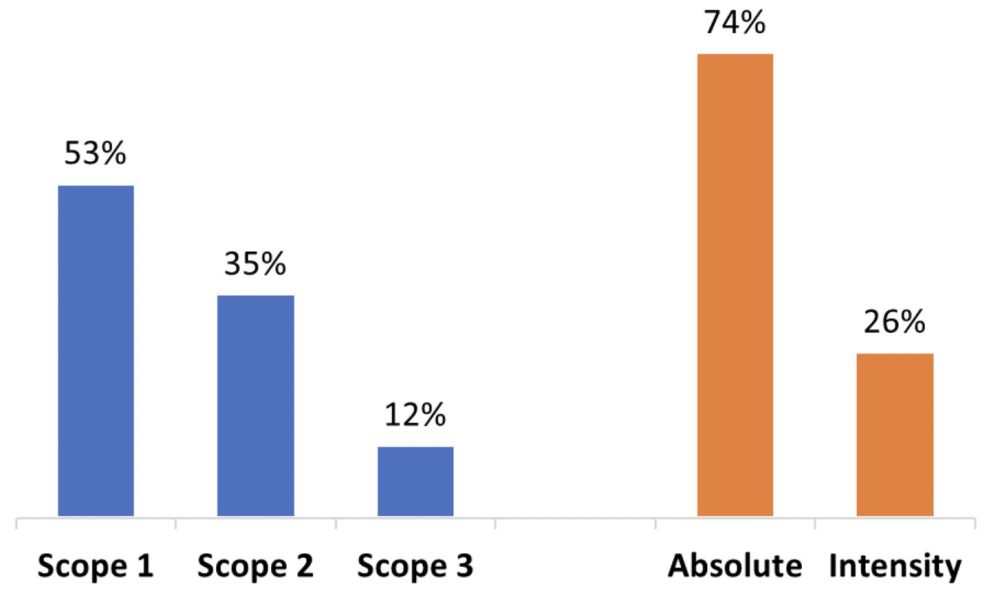

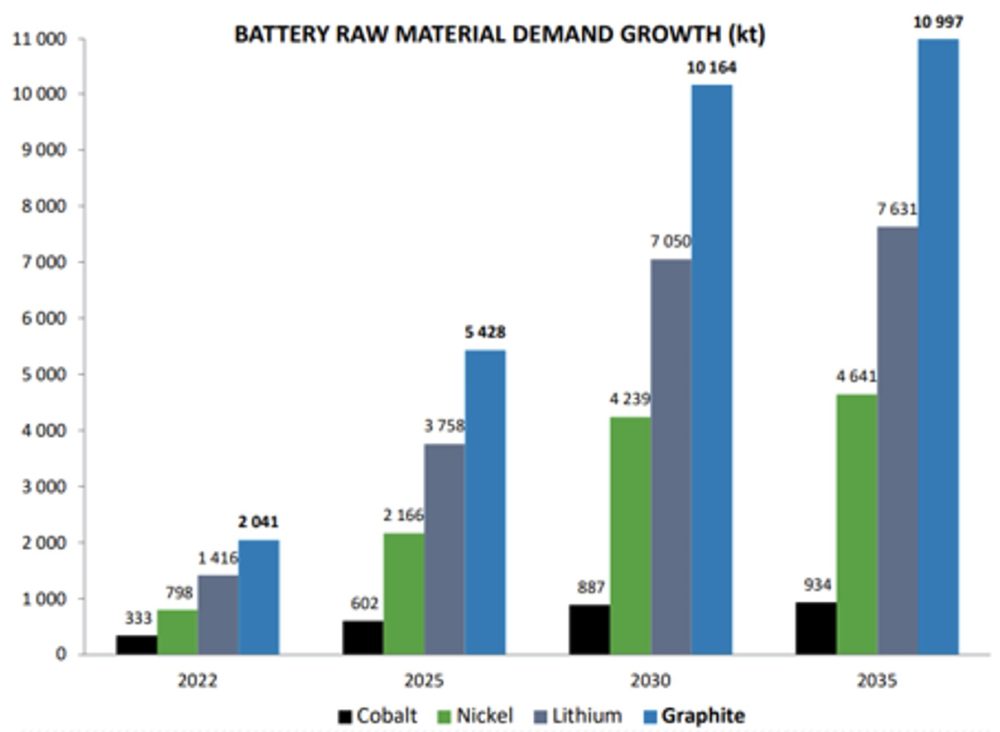

EVs require certain critical minerals that internal combustion engine (ICE) vehicles do not, such as lithium, cobalt, graphite, nickel and others as components for their batteries. Based on market expectations for EV adoption, battery metals are expected to require significant supply growth in order to meet demand expectations. The annual growth rates in demand for most battery metals including lithium, graphite and cobalt are in the 5-10% range, which is unprecedented. Let us not forget the uranium needed for nuclear power plants, which will be required to increase the base load power supply.

Source: Benchmark Mineral Intelligence, May 2023

In addition to cobalt, nickel, lithium and graphite, the world will need more copper for wiring. EVs have a higher copper intensity than ICE vehicles and will be required for the build- out of charging infrastructure. According to CRU and BMO Capital Markets, copper content per light duty vehicle is 3-4x the amount per current ICE vehicle, with next generation EVs hoping to get that down to 1-3x by 2030 [1]. By 2030 total vehicle demand for copper between EVs and ICE vehicles is expected to double [2].

Raw material availability will set the pace and the mining industry may struggle to deliver

In a transition of this scale, there will be setbacks that disturb the supply-demand balance. Production growth along the value chain will need to be synchronized to avoid constraints . The issue is that mining capacity has a long lead time and is on a different timeline to global battery demand, EV charging station capacity and even EV penetration. It takes 2-5 years to build a battery plant, while mines require 5-25 years to develop. For this reason alone, the road towards lower emissions may be bumpier than people expect.

Today, China dominates every segment in the battery supply chain and political tensions are accelerating. In response, Western governments are scrambling to be self-sufficient and independent. The U.S. Inflation Reduction Act (IRA) is the most publicized legislature geared towards security of the energy transition value chain, but other counties are following suit. Effectively, there will likely be two parallel markets for many of the critical metals, and the West will need to catch-up.

Raw material extraction is always complicated but there is additional complexity associated with the growth rates required for energy transition. For instance, processing of critical metals is often problematic, as there is a uniqueness to each deposit which requires advanced engineering. Many of the metals are also located in jurisdictions with geopolitical risk, which adds an extra layer of uncertainty. Overlaying risks, including the lack of technical expertise, will potentially compromise the ability to meet demand.

Obtaining permits can also be extremely complex and time consuming. Today’s world has a heightened focus on Environmental, Social License and Corporate Governance (ESG) factors and new mining projects cannot be rushed through for the sake of satisfying any urgency on the demand side. The industry will need to ensure that all aspects of their mining projects are satisfied.

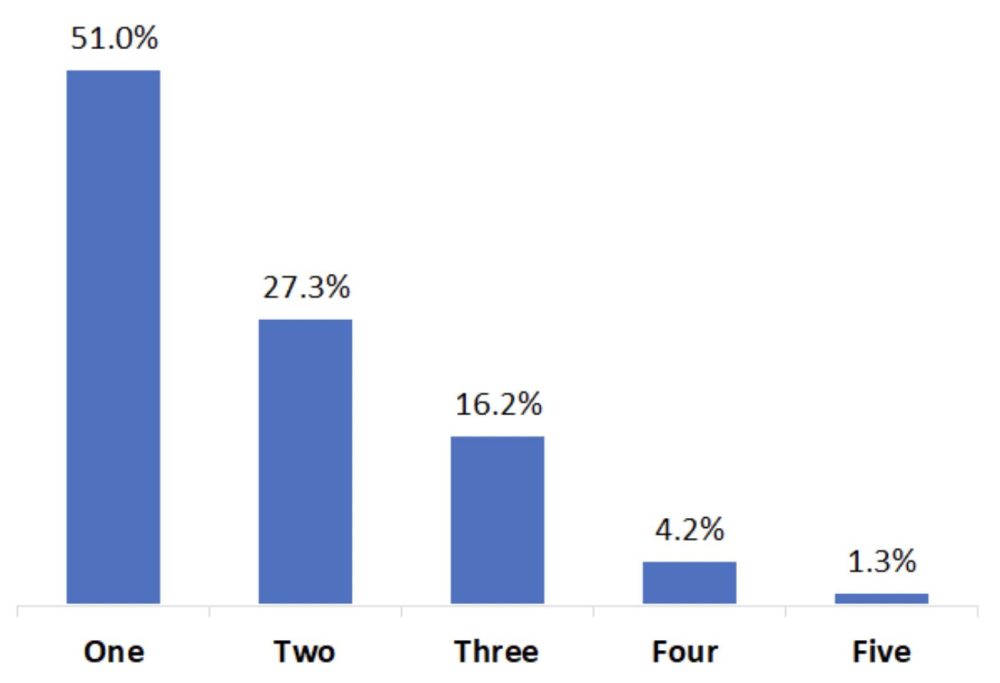

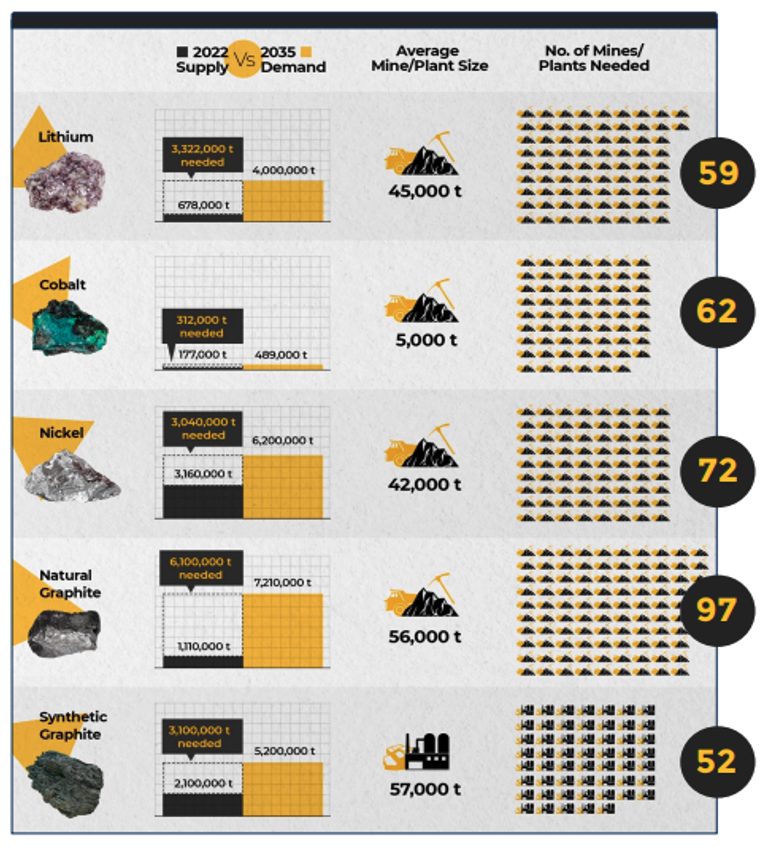

Another startling metric outlined by Benchmark Mineral Intelligence (BMI), an industry think tank, is the number of new mines that will be required to supply the planned battery gigafactories. BMI estimates that between now and 2035 the planned battery plant capacity will require ~ 50-100 new mines to be built in each of the key battery metals. The industry has never seen growth rates like these [1].

Source: Benchmark Mineral Intelligence

The investment opportunity

Investing in this complex and dynamic environment is difficult, but the opportunities are meaningful and this, we believe, will keep investors drawn to the space. Most importantly, the growth in demand is significant and necessary with enormous capital needs. This is a multi-decade global transition at its infancy and, as this dynamic environment evolves, there will be significant investment opportunities, as well as benefits for society.

BMI calculates that at least $514 billion will be required by 2030 to facilitate a 3.7x facilitate increase in storage capacity. An additional $406 billion will be required between 2031-2035 [1]. Wood Mackenzie, meanwhile, forecasts a total investment of US $1.2 trillion by 2050 to achieve the Accelerated Energy Transition (AET) -1.5-degree Celsius climate change target [3].

It is highly unlikely that the individual supply chain components will increase in tandem. As the world scrambles to transition quickly, there will likely be surpluses and shortages at any point in time. Therefore, diversification through all parts of the supply chain is a prudent approach.

We evaluate potential investment opportunities based on technical quality of the projects, quality of the management and economic robustness. Our active approach to investing in the mining industry can help contribute to overcoming some of the challenges while generating attractive returns for our investors.

Sources

[1] Thunder Said Energy

[2] BMO Capital Markets

[3] Benchmark Mineral Intelligence