A Simple Framework for Selecting and Integrating ESG Data

July 29th, 2020 | Mackenzie Hargrave

Top-down management of an equity portfolio involves analyzing major market segments, such as regions, countries and sectors.

Security selection plays a decidedly secondary role. Yet, responsible equity investment is based mainly on information specific to individual securities, namely the increasingly mainstream ESG criteria. That being said, there is nothing to prevent managers who use a top-down approach from implementing credible responsible investment. We propose to do so by building investment universes that are consistent with managers’ decision-making levers and ESG-related objectives.

For a top-down strategy to be implemented in an investment universe, this universe must be representative of the reference market. Take the example of managers who want to invest in European banks. Their primary objective is to invest in a representative subset of the European banking industry. Exposure to the subset is more important than selection of individual securities. This principle is generally applicable to all the decision-making levers specific to top-down management. Thus, all the major segments of the reference market (geographical and sectoral) should be well represented in the investment universe.

The ESG criteria are numerous and varied: they include carbon footprint, water intensity, board independence, workplace mortality rate and so on. To guide the construction of a responsible investment universe, it is important to set precise and measurable objectives.

The objectives are used to evaluate the selected methodology. Does it truly enable the managers to meet their responsible investment targets? Representativeness of the reference market, referred to above, is a requirement that often leads to application of ESG criteria by market segment, occasionally with undesirable or unexpected effects.

Carbon footprint is a prime example of a criterion whose application by market segment can prove problematic. Managers who remove 200 securities from a global index by targeting the largest emitters by market segment reduce the carbon footprint per billion dollars invested from 94 tons to 55 tons. Even so, four of the world’s 10 largest emitters are still present because, despite their mediocre performance relative to the broad market, they stand out in their sector of activity. What is acceptable to one investor may be unacceptable to another – hence the importance of setting clear objectives.

While the previous example calls for the development of specific objectives, it also illustrates the importance of ensuring that the selected methodology can achieve them. We think a methodology that combines global divestment filters and market segment filters gives managers sufficient flexibility to construct investment universes that combine the requirements of top-down management with varying degrees of ESG integration intensity.

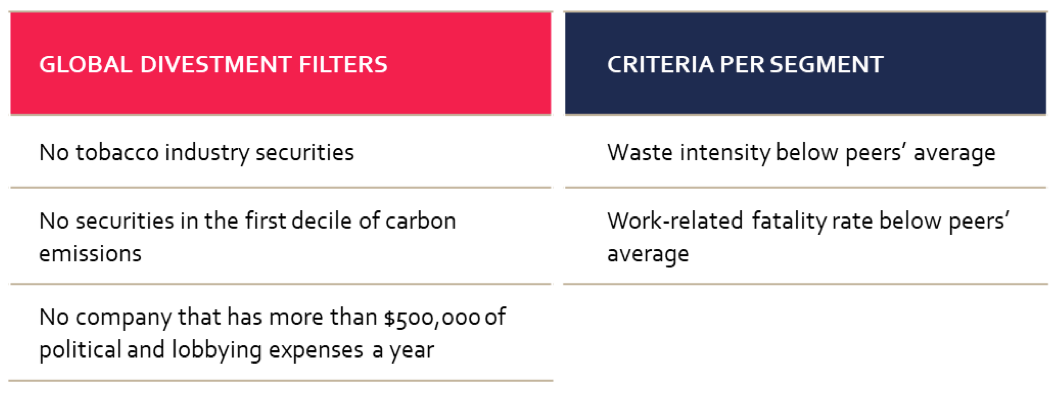

Eliminating all tobacco industry securities is an example of a global divestment filter. It guarantees the best possible performance in terms of this specific ESG criterion, but at the same time it eliminates the decision-making levers, namely the allocation to this industry and the stock selection within the industry. The use of global divestment filters should therefore be limited to those ESG criteria on which the manager or the client is not willing to compromise.

As for market segment filters, they are designed to select those companies with the best performance relative to their peers. Thus, they do not eliminate segments of the reference market or decision-making levers. They usually offer a good compromise between ESG objectives and management requirements.

Let’s take the example of an investment universe applied to the developed country equity market and apply three divestment filters and two criteria per segment.

Table 1

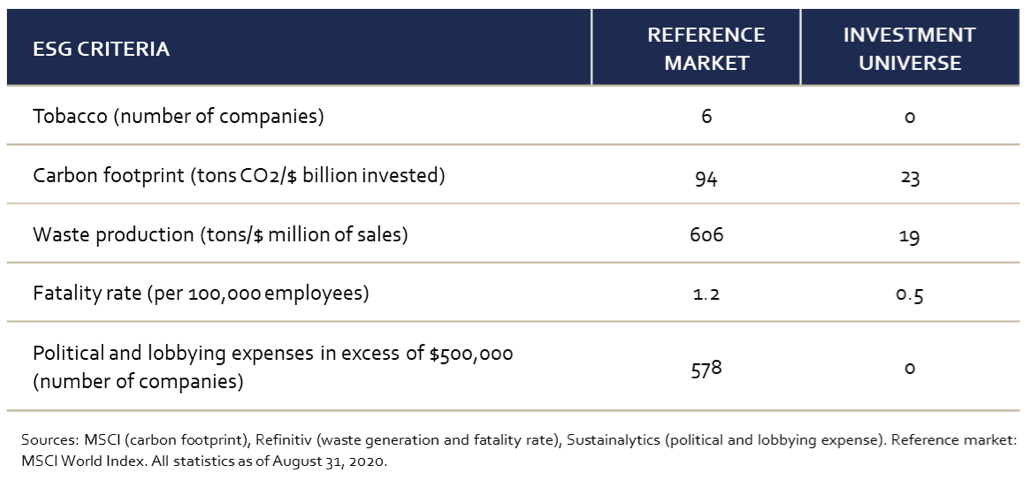

The analysis of the resulting investment universe should answer two questions:

Table 2 answers the first question in the affirmative. For all the ESG objectives selected, the investment universe gets a much better rating than the broad market.

Table 2

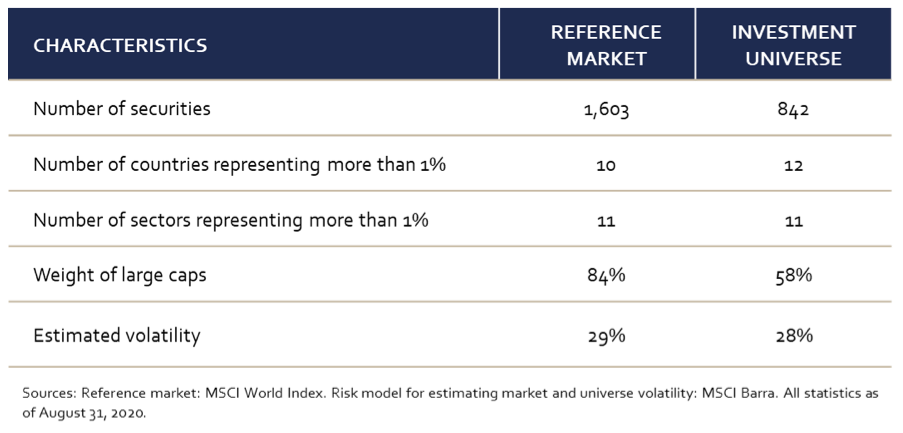

We can conclude from the figures in Table 3 that a top-down strategy could be deployed in this universe. All sectors are well represented, and the number of well-represented countries is even higher than that of the reference market. The relative importance of large caps is sufficient and the estimated volatility is similar to that of the reference market.

Table 3

This simple example shows that top-down managers can achieve ambitious ESG objectives while allowing themselves enough decision-making leeway to implement their investment strategy.