Energy End Users May Be the Missing Piece of Your Sustainable Portfolio: Interview with Andrew Simpson

December 20th, 2024 | Andrew Simpson

If you’ve been following the headlines this year, you might think climate action is stalling. Political noise, policy reversals, and targeting of investors and their collaborative climate initiatives, have dominated the narrative.

Yet, beneath the surface, the structural forces driving decarbonisation are stronger than ever. From the United States to China, 2025 has been a year of quiet progress.

For investors, this is not just a story of resilience—it’s a validation of a multi-decade structural growth opportunity.

Despite President Trump’s rhetoric and anti-climate catchphrases — notably the ‘green new scam’ — his signature One Big Beautiful Bill Act (OBBBA) was better than feared. While the generous electric vehicle credits were scrapped and renewable developer credit timelines were shortened, much of the Biden-era Inflation Reduction Act (IRA) has remained intact.

And thanks to grandfathering rules being left largely intact by Trump, developers like NextEra Energy can continue to take advantage of the Biden-era credits to 2030. [1]

Despite the policy rollback, the decarbonization of the U.S. power sector is continuing. In February, as Trump resumed office, the U.S. Energy Information Administration predicted that over 90% of new utility-scale capacity additions would be renewables and battery storage. [2]

Despite the noise since then, the latest data to August from regulator FERC shows that solar and wind represented 88% of all new capacity additions. [3]

Source: FERC

This is not a blip—it’s a structural shift. Competitive costs and the rapid speed of deployment are driving a clean energy build-out that the latest policy reversal has not stopped.

Both gas and nuclear will remain part of the long-term mix, but neither can scale quickly. For gas, while there is certainly more demand, a turbine order made today will not be online until the 2030s.

And while nuclear has seen strong interest, including from AI-linked names like Microsoft, Google, Meta and Amazon who want baseload carbon-free power, so far, we have mainly seen restarts of recently mothballed plants. New small modular reactors (or SMRs) remain a 2030s story.

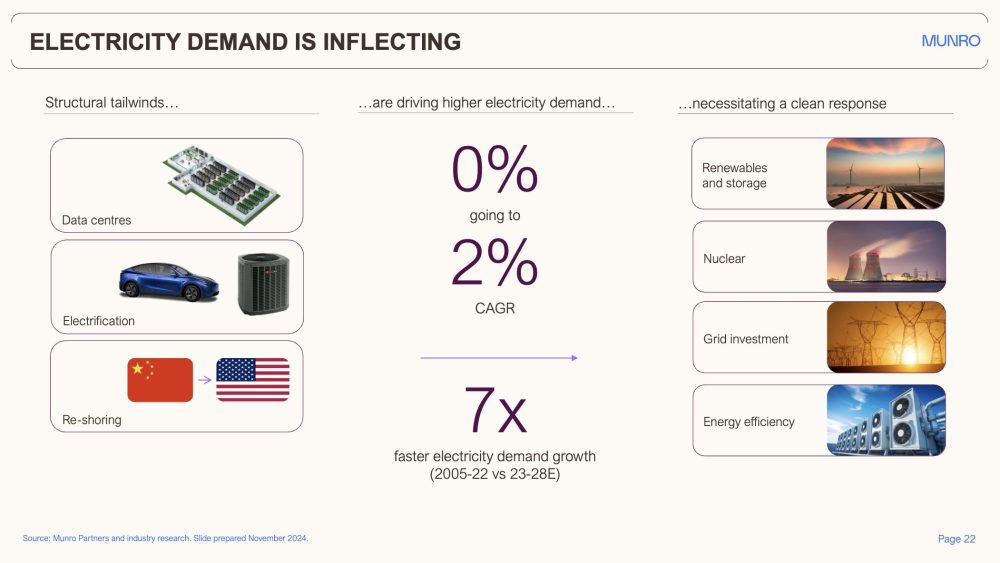

At the same time as supply is greening, demand is inflecting. After decades of flat growth, where new demand for electricity was offset by efficiency gains, today we’re seeing absolute demand rising.

Why?

We’ve observed three structural drivers:

In fact, we surmise that the U.S.’s strategic desire to lead in AI and to reshore from China explains why Trump’s policy rollback for renewables was more benign than anticipated. The Administration realises the U.S. needs all the electricity it can get.

The result: U.S. electricity demand is projected to grow much faster now than the last 2 decades. This presents a structural tailwind for utilities, grid and renewables developers, and service providers.

Source: Munro Partners and industry research. Information prepared November 2024.

There are many ways to invest in the ongoing structural greening of the U.S. grid and the recent inflection in demand. Quanta Services, a holding in our Global Climate Leaders strategy, is a prime example.

Quanta specialises in developing grid infrastructure and renewables projects. With nearly US$40bn in backlog and long relationships with major developers, the company is well positioned to capture increasing spending on the grid and renewables.

In early 2025, President Trump again pulled the U.S. out of the 2015 Paris Agreement on climate change, but the global response was telling: like last time, no one followed. The other 194 signatories remain committed.

Today, even without the U.S., countries representing around three quarters of global GDP and emissions are committed to net zero.[5] In many cases, they are accelerating their efforts.

China remains the world’s largest emitter with an estimated 29% contribution to global emissions in 2024, according to the European Commission. [6]

With our newsfeeds centred around what was happening in the U.S., it was easy to miss China’s first absolute emissions reduction target announced in September: 7–10% below peak levels by 2035.

Critics argue this is modest, but scale matters: cutting 2024 emissions by 10% in China is equivalent to fully decarbonising Canada not once, but twice! [7]

Alongside this, China aims to raise non-fossil energy consumption to 30% and expand wind and solar capacity to 3,600 GW by 2035. Again, to get a sense of the scale, that’s more than three times the entire electricity generation capacity of the U.S. (at 2023 recorded levels). [8]

Again, this presents an enormous opportunity for the companies that will make this happen, and for their investors.

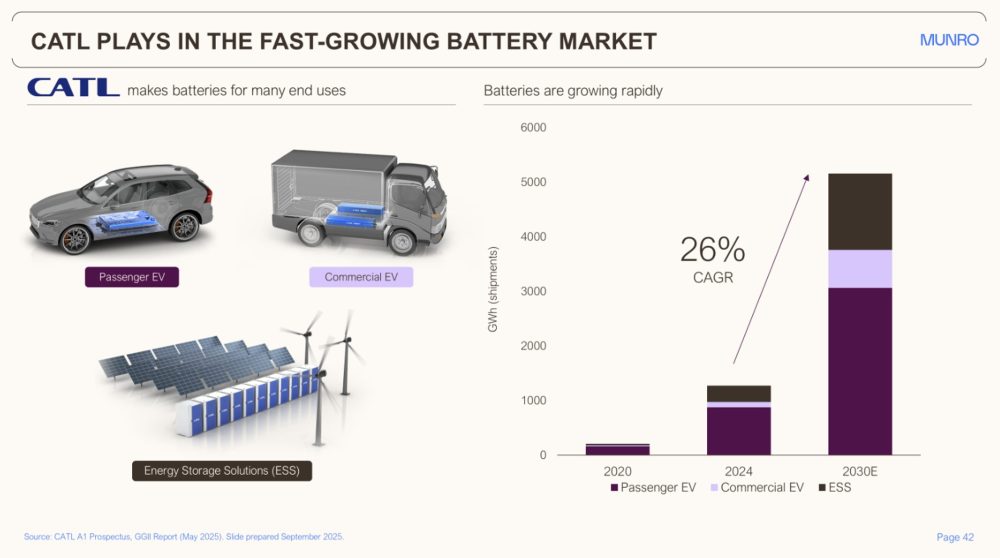

China’s renewable ambitions hinge not just on solar and wind but on energy storage solutions (or ESS). China needs ESS because much of the solar it has already installed is curtailed (essentially wasted) because supply exceeds demand.

To illustrate, in the first half of this year, 33% of the solar generated in the western Chinese region of Tibet was curtailed. If they had more ESS, they could store this excess supply during daylight hours and use it in the evening peak.

To address this, China recently announced ambitious ESS policies aiming to grow capacity by nearly 30% p.a. to 180GW by 2027, requiring investment of US$35b: a huge revenue opportunity for developers and battery makers. [9]

Contemporary Amperex Technology Limited (CATL), another Global Climate Leaders strategy holding, is riding this wave. A Chinese national champion, CATL holds the largest global market share — over a third — in batteries today. They now predict that the growth in batteries for ESS will outpace electric vehicles to the end of the decade.

Source: CATL a1 Prospectus, GGII Report (May 2025). Charts prepared September 2025.

2025 has been a year of contradictions. The headlines scream rollback, but the reality on the ground whispers resilience and inflection.

In the U.S., the reality is that even today renewables are being deployed much more than fossil fuels. The dearth of cheap, fast-to-deploy and available alternatives, and the inflection in electricity demand, provide ongoing support.

Outside the U.S., we see decarbonization ambition is increasing. China’s aim to take two Canadas-worth of emissions out of its system by 2035 presents investors an opportunity to invest in – and benefit from – a generational transformation.

For those willing to look beyond the headlines, 2025 is not a setback for climate investing — it’s validation of a robust multi-decade structural growth opportunity.

Sources:

[1] NextEra Q3 2025 results presentation

[2] https://www.eia.gov/todayinenergy/detail.php?id=64586

[3] https://cms.ferc.gov/media/energy-infrastructure-update-august-2025

[4] Per Ember data https://ember-energy.org/data/yearly-electricity-data/

[6] https://edgar.jrc.ec.europa.eu/report_2025

[7] In 2024, Canada’s emissions were 768 mtCO2e, and 10% of China’s emissions was 1,554 mtCO2e https://edgar.jrc.ec.europa.eu/report_2025

[8] In 2023, the U.S. had 1,189 GW of generation capacity: https://www.eia.gov/energyexplained/electricity/electricity-in-the-us-generation-capacity-and-sales.php#:~:text=At%20the%20end%20of%202023,electricity%2Dgeneration%20capacity%20in%202023.

[9] UBS

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.