Houses washed away by floods, power lines and road surfaces buckling under extreme heat, and drought threatening food supplies and pressuring water resources. These natural disasters are becoming all too common. And they are taking a massive economic toll.

In 2024 alone, the world experienced more than 150 extreme weather events, causing an estimated USD320 billion in global economic losses – 40% higher than the decade-long annual average.

As the impact of climate change and environmental degradation increases, it is clear that investing in adaptation and resilience (A&R) – concrete steps such as enhancing grid resilience through advanced modelling and simulation, retrofitting existing buildings with efficient energy technologies or installing stormwater pump stations – becomes just as important as measures to mitigate global temperature rises.

Crucially, A&R investment is more than just about blunting the immediate impact of climate change while taking advantage of the potential for attractive return.

Companies that can meet the growing demand for climate change adaptation with the right business model and economics have a real chance to offer attractive investment opportunities.

Inflection point

Until now, adaptation has not been a magnet for investment.

The sector attracted just over USD30 billion in new capital in 2024, falling well short of hundreds of billions of dollars experts estimate are needed to mitigate the financial impact from climate change in the coming decades.

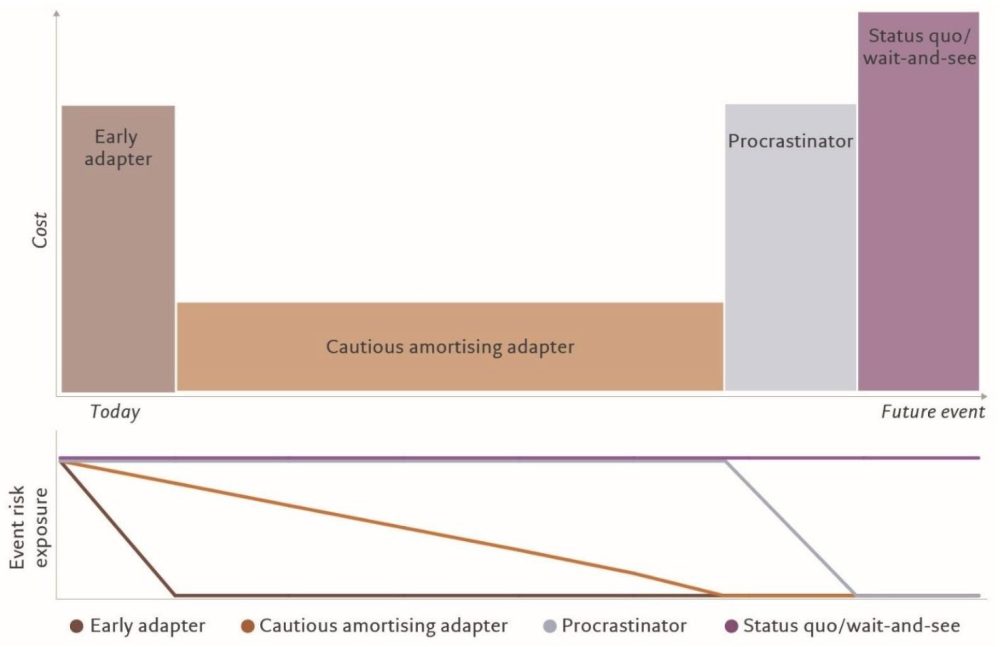

The lack of corporate commitment may be down to a potential dilemma or trade-off – the earlier you are, the more uncertainty there is. Corporates do not want to overspend on things they do not know and they tend to wait. But the longer you wait, the greater your exposure becomes to future risks.

Figure 1 – Adapter’s dilemma

Sample management approaches to climate adaptation

Source: JP Morgan, Building Resilience Through Climate Adaptation, 2025

Encouragingly, this gap is beginning to close.

According to a report by London Stock Exchange Group, 34% of large and medium-sized listed companies in the FTSE All World Index are already referring to adaptation measures in their annual disclosures.

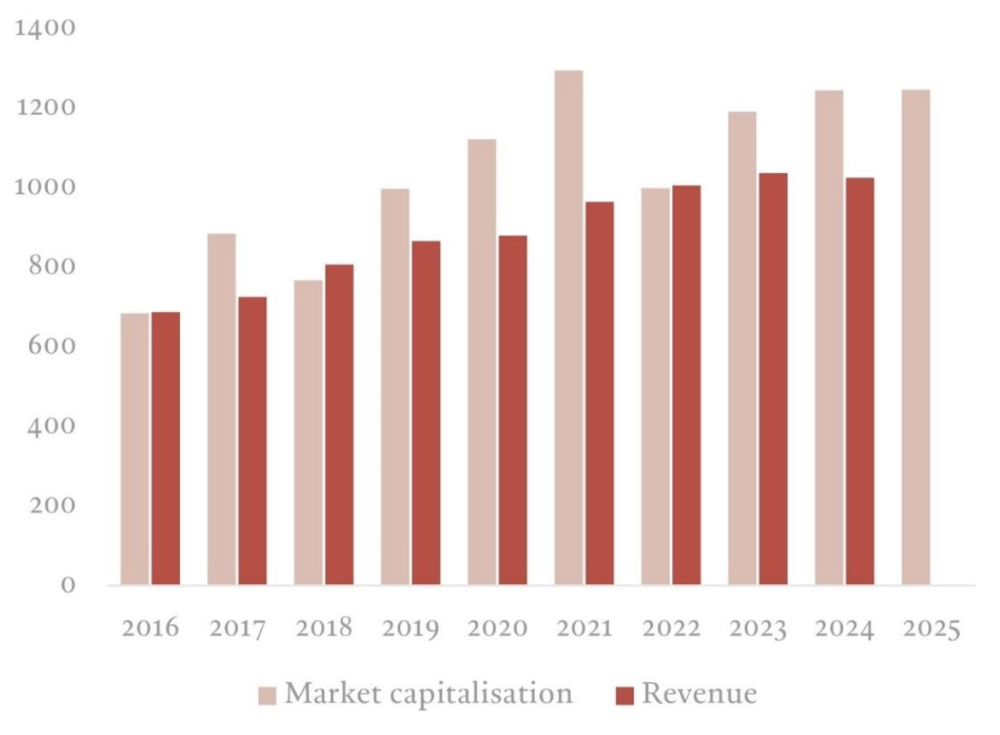

Corporate adaptation finance flows are growing at a four-year Compound Annual Growth Rate (CAGR) of 21% with companies who have embraced adaptation solutions generating over USD 1 trillion in green revenue last year.

Fig. 2 Adaptation and resilience growth and sectors

Market cap and revenue growth of adaptation and resilience industry (USD billion)

Source: LSEG, data as of 12.05.2025

A conservative estimate from climate consultancy Tailwind assumes that if each of the 10,000 publicly listed companies spends just USD 50 million on climate resilience investments, the latent demand from corporations should be at least USD 500 billion annually. [1]

Technology companies are among the leading industries investing in A&R strategies. That is because extreme heat, drought and flood risks threaten their operations.

Those building and operating data centres in arid regions like Arizona will need to consider investing in efficient cooling technologies, large solar panels, smart water management and recycling systems, as well as adopting sustainable and green building designs.

These measures should not only mitigate drought and heat risks and ensure round-the-clock operations during extreme weather but also reduce emissions. By conserving energy and water, they will ease strain on local grids and water systems, on top of cutting utility bills.

A study by the World Resources Institute (WRI) found that every USD 1 invested in A&R generates more than USD 10 in benefits over 10 years. This translates to potential returns of over USD 1.4 trillion, with average annual returns of 27%. Part of this will accrue directly to investors.

Crucially, these benefits go beyond financial gains. The report also explained that A&R projects typically yield a “triple dividend,” providing an environmental and social return in addition to a financial one.

The WRI study found that financial and non-financial gains from A&R projects are often equal in magnitude, yet only 8% of investment appraisals translate every benefit, financial and non-financial, into a single dollar figure. This suggests that societal rates of return are substantially underestimated in economic assessments of most adaptation investments.

A&R investing therefore stands out as a powerful way to protect assets, unlock new sources of growth and capture attractive return potential while helping build a more climate-resilient economy for the decades ahead.

Sources

- Tailwind, Taxonomy for Climate Adaptation and Resilience Activities, 2024

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.