The market share of responsible investment (RI) assets under management (AUM) in Canada has grown significantly, according to the latest findings from the 2024 Canadian Responsible Investment Trends Report.

The 2024 Report reveals a pivotal milestone for the industry, with RI now accounting for 71% of total AUM. This growth is accompanied by a marked rise in investor confidence, driven by clearer definitions of RI strategies and improved ESG reporting practices.

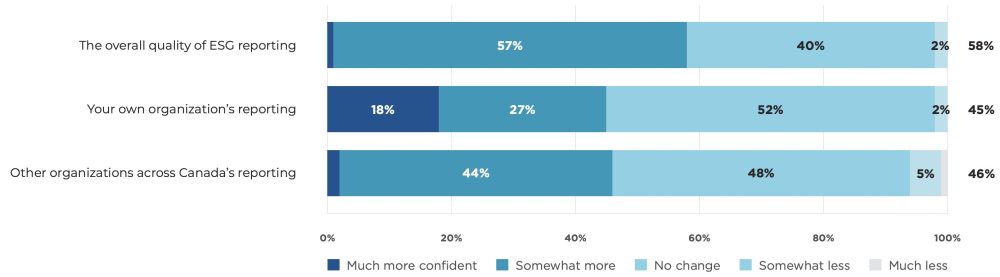

For the second year in a row, close to 60% of respondents say they are more confident in the overall quality of reporting than they were last year. And in each category of ESG reporting that was measured, only 6% of respondents, or fewer, expressed less confidence than last year. When asked what would further increase their confidence in reporting, respondents noted that more universally accepted frameworks, alongside standardization and auditing of reporting, would be helpful.

Confidence in Reporting of RI AUM and Specific RI Approaches

Source: 2024 Canadian RI Trends Report

“As responsible investing continues to evolve, we cannot become complacent,” says Patricia Fletcher, CEO of the Responsible Investment Association. “Collective action and advocacy are necessary to further advance the adoption of RI and mobilize capital to strengthen Canada’s economic resilience.”

A window of opportunity exists to further strengthen RI in Canada, and this will require collective action and advocacy. Standardization is needed to further improve confidence and unlock the value that RI brings to investment decision-making. Recent definition changes have increased confidence, but more changes and standardization are on the horizon, and the industry must continue to adapt.

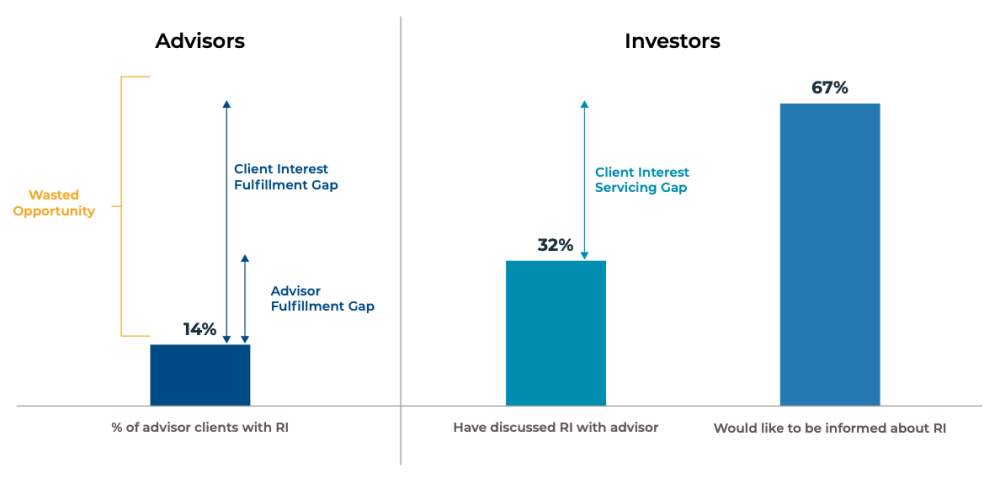

In 2023, 65% of surveyed Canadian investors expressed interest in responsible investment (RI), and two-thirds of respondents (67%) would like their financial services provider to inform them about RI options that are aligned with their values. However, only one third of those surveyed reported that their advisors are initiating discussions around RI, indicating a significant service gap. Year after year this service gap persists, leaving a full third of investors eager to speak to a financial service provider about responsible investing. With such clear client demand, why are so many financial advisors sitting on the sidelines of responsible investment?

– Reasons not to offer RI centre around a lack of knowledge and resources, or a perceived administration burden. Product availability is not a barrier.

– Advisors’ education and knowledge of RI are tightly linked to their overall use of RI. The more confident they are about RI, the more extensively they will use it in their practice.

– Advisors rely on investment companies – especially wholesalers – for information, and will likely turn to them with questions when introducing or increasing their RI usage.

– Investor demand is driving advisor adoption.

– Nearly 90% of RI users anticipate the growth of RI over the coming years, and non-users are open to using RI.

This means that financial advisors who learn to engage clients on ESG topics and RI strategies stand to gain tremendously.

Client and Advisor Fulfillment Gaps

Source: 2024 Advisor RI Insights Study – Topline Report

How can we drive greater adoption of RI at the retail level? It will take a 360-degree approach, from advisors informing themselves and servicing their clients based on needs and priorities, to fund manufacturers and wholesalers providing the needed support.

It is clear that the more RI knowledge an advisor has, the better positioned they are to serve their clients’ ESG-related needs and narrow the RI service gap. These recordings from the 2024 Advisor RI Bootcamp present an excellent jumping off point for anyone looking to learn about leading responsible investment products from the portfolio managers and analysts behind them.

And if you would like to learn more about RI assets and trends in Canada, be sure check out the virtual launch of the 2024 Canadian RI Trends Report on November 19th.

The opportunity is there – but it is incumbent on all of us to play our part in closing the RI service gap.

For more information about the 2024 Advisor RI Insights Study, contact membership@riacanada.ca.

In March 2024, the U.S. Securities and Exchange Commission (SEC) enacted the legislation that would require U.S.-listed companies to publicly report their climate-related risks and impacts. The long-awaited SEC Climate Disclosure Rules were released following months of intense public debate (including fierce opposition) and a record 24,000 comments submitted by companies, investors, auditors, legislators and other groups.

Now, and for the first ever time in the U.S., corporate climate disclosures would become mandatory in SEC filings and would be subject to the same level of scrutiny and audit requirements as for financial statements – ultimately putting climate disclosures on par with financial disclosures. In doing so, this groundbreaking ruling was intended to help make these climate disclosures “more reliable” and “provide investors with consistent, comparable, decision-useful information, and issuers with clear reporting requirements,” according to Gary Gensler, the SEC Chair.

However, the SEC made key omissions, including most notably, dropping requirements for the disclosure of value-chain emissions, otherwise known as Scope 3.*

*Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly affects in its value chain.

Scope 3 emissions represent one of the Grand Challenges of Net Zero, and what the London Stock Exchange Group calls “one of the most vexing problems in climate finance.” These emissions are broad, spanning multiple sources upstream and downstream of company operations, and often across multiple tiers of suppliers and customers. They are also complex, as Scope 3 emissions are both costly and challenging to estimate, let alone measure directly. And often, they represent the overwhelming majority of a company’s overall emissions footprint. Increasingly, Scope 3 also represents a major obstacle for investors who are looking to cut financed emissions across their portfolios and meet net-zero commitments.

By excluding Scope 3, the SEC ruling has prompted companies and investors to wonder if this would be the end of Scope 3 disclosures for U.S. issuers and for corporate carbon accountability.

Scope 3 disclosures are on the rise, globally and in the U.S.

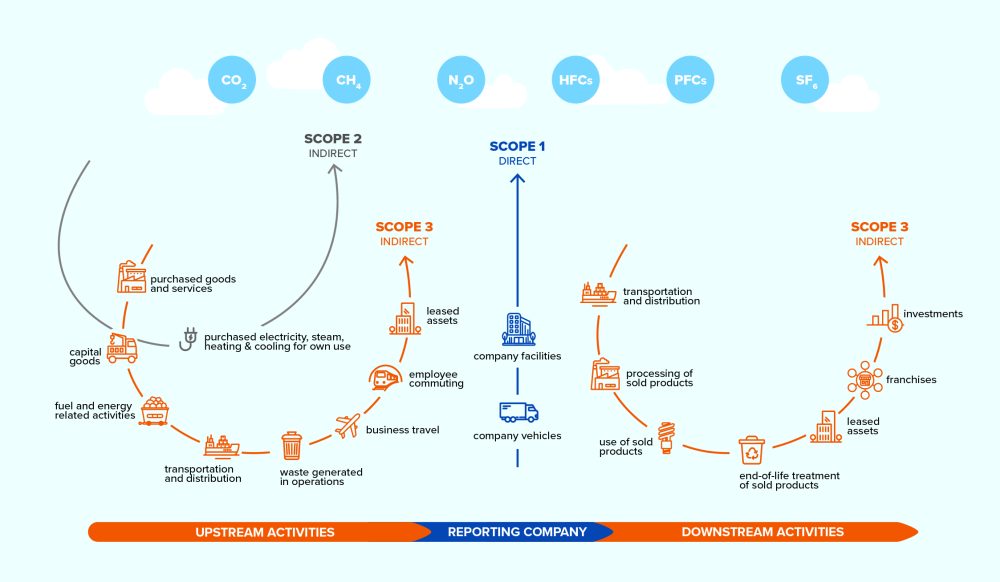

Here is a quick primer on Scope 3. Within carbon accounting, greenhouse gas (GHG) emissions are divided into three discrete ‘scopes’ based on where the emissions are created across a company’s operations and its wider value chain—as shown in Figure 1.

While companies have more control and influence over their Scope 1 and 2 emissions, Scope 3 emissions are generally more significant and result from companies’ supply chains (‘upstream Scope 3’) and use of companies’ products by consumers (‘downstream Scope 3’). Scope 3 is more complex for companies to track or estimate, but if gone unmanaged, may present financial risks, ranging from declining product competitiveness as consumer awareness for global warming increases, to higher cost of capital as insurers and investors aim to manage their own exposure.

Figure 1: Overview of GHG scopes and emissions across the company value chain.

Given the complexity and wide reach of these emissions, it comes as no surprise that globally, fewer companies report on Scope 1, 2 and 3 emissions, as compared to on Scope 1 and 2 alone – and U.S.-based companies in particular tend to lag on Scope 3 reporting.

However, the number of companies, both globally and in the U.S., that are reporting on their Scope 3 emissions has been consistently increasing year-over-year. According to the MSCI Net Zero Tracker, as at January 2024, approximately 42% of listed companies globally disclosed at least some of their Scope 3 emissions – a 17% increase compared to two years ago.

This disclosure trend is echoed by CDP. Of the 1,077 U.S.-based companies that reported on the CDP Climate Change questionnaire in 2023, only 13% did not report any Scope 3 emissions.

We see this trend reflected within our Mackenzie climate action engagements across U.S.-based issuers. Of the 100 companies with whom we engage via Mackenzie’s thematic climate engagement program, 41 are U.S. based, and of these companies:

– 44% have committed to SBTi (Science Based Target initiative) or set a SBTi validated target – 41% have set GHG targets that include Scope 3 emissions – 73% report in line with TCFD (Taskforce for Climate-Related Financial Disclosures) – 76% report to CDP

From our climate engagement discussions, we are seeing a modest but consistent year-over-year increase in Scope 3 emission disclosure. Listed below are some notable examples of U.S. companies leading the way on disclosing and abating Scope 3 emissions.

Ahead of the pack: U.S. companies leading on Scope 3 disclosure, based on Mackenzie’s climate engagements

Marathon Petroleum Corp. (MPC) is a leading integrated, downstream energy company, based in Findlay, Ohio. Marathon reports on Scope 3 Category 11: Use of Sold Products,* which is the largest source of the company’s overall Scope 3 footprint. In addition to this, Marathon has also set a 2030 target to reduce absolute Scope 3 Category 11 emissions by 15% below 2019 levels on refined product. This target is informed by methodologies devised by the SBTi and Ipieca,** and aims to demonstrate the competitiveness of Marathon’s business within the global market.

Linde PLC (LIN) is one of the world’s largest industrial gases (such as ammonia and hydrogen) and engineering companies that is helping enable the clean energy transition. With operations spanning more than 80 countries, including the U.K. and the U.S., Linde is subject to various climate disclosure rules globally. Therefore, it’s not surprising that Linde currently reports on 14 categories of Scope 3 emissions representing all relevant categories for Linde. –About 40% of this inventory has been verified by a third party to the limited assurance level. Linde has set a SBTi-validated target to reduce its Scope 1 and 2 emissions and is working on emissions estimation and methodology development in anticipation of setting additional Scope 3 emissions reduction targets by 2026.

WEC Energy Group Inc. (WEC) is one of the largest electric generation and distribution and natural gas delivery group of companies in the U.S., based in the Midwest. WEC recently undertook an extensive review of all 15 categories of Scope 3 emissions across their organization to build the company’s first Scope 3 inventory. The disclosure was a cross-functional effort, relying on subject matter experts across WEC’s supply chain, finance, gas distribution, fuels, energy efficiency and environmental teams, and overseen by a dedicated Scope 3 Executive Steering Committee. WEC currently discloses multiple categories of Scope 3 through its ESG reporting.

*Per the GHG Protocol, emissions classified as Scope 3 – Category 11: Use of Sold Products are the GHGs emitted during the use of a company’s sold products [Source: GHG Protocol (2013) – Technical Guidance for Calculating Scope 3 Emissions (V1.0)].

**Ipieca is a global not-for-profit, oil-and-gas industry association for environmental and social issues.

Based on public disclosure and our own experience, company efforts to disclose and abate Scope 3 emissions continue even as the SEC removes its focus on Scope 3.

What’s driving this increased disclosure?

These emissions disclosure trends are being driven by several factors, but most notably by the shifting regulatory landscape around Scope 3 and the rise of climate disclosure rules globally.

During the two years that the SEC spent deliberating on the final rules, a suite of climate disclosure rules and standards emerged, all of which included provisions for the disclosure of emissions across a company’s Scope 1, 2 and 3. In 2023, the European Union’s (EU) Corporate Sustainability Reporting Directive entered into force, the International Sustainability Standards Board released its IFRS S2 standard, and the state of California passed the S.B. 253, the Climate Corporate Data Accountability Act.

We operate in a globalized economy – companies have global value chains, global consumers and global investors. Rather than seeing a form of ‘accounting arbitrage,’ and a race to the lowest level of disclosure when it comes to emissions reporting, what we predict is increased disclosures for companies that operate globally. Texas-based firms doing business in California or in the EU, for example, may now be required to disclose their Scope 3 emissions, regardless of the SEC final ruling.

We see this divergence in Scope 3 disclosure rules between the U.S. and other parts of the world as analogous to the longer-standing divergence between the US Generally Accepted Accounting Principles (US GAAP) and International Financial Reporting Standards (IFRS), where the U.S. decided to maintain their own accounting standards.

In the early 2000s, the International Accounting Standards Board released a new accounting standard, the IFRS, which was intended to establish global common accounting standards. However, the U.S. continued following US GAAP, leaving many U.S. issuers to report in adherence with both GAAP and IFRS.

The direction of travel on Scope 3 disclosure is more, not less

We believe a notable paradigm shift has emerged regarding Scope 3 emissions reporting. Even if the SEC has dropped requirements for mandatory Scope 3 disclosure, U.S. issuers choosing to access global investors and supply chains will be required to adopt international climate disclosures. Ultimately, this leads us to believe that the direction of travel on Scope 3 disclosure is likely to be more, not less.

Contributor Disclaimer

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document includes statements that may be considered forward-looking information. Forward-looking statements are not guarantees of future performance or events, and involve risks and uncertainties. Do not place undue reliance on forward-looking information. In addition, any statement about companies is not an endorsement or recommendation to buy or sell any security. The content of this policy (including facts, views, opinions, recommendations, descriptions of or references to products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Investing in India’s rapidly developing economy offers a promising opportunity for substantial returns, yet it also presents unique challenges. As the world’s most populous country and one of its fastest-growing markets with over 4,400 listed companies, India is drawing attention in the global investment landscape. Investments are pouring into the country from institutions as well as the retail arena; some increasing their existing allocation, others making a dedicated initial allocation to the country while others are diversifying or fully divesting from their existing China exposure and into India.

India’s economic growth story is compelling. With a population over 1.4 billion, a rapidly growing middle class and robust economic reforms, India is poised for substantial growth, setting the stage for the domestic economy to thrive. Approximately 40% of India’s population falls within the age group of 18 to 35 years (the highest Gen Z and Millennial ranking in the world) which is propelling the consumer markets and is the major driver of economic growth and development regardless of events in the USA or elsewhere in the world.

India’s infrastructure is rapidly preparing for decades of growth, with examples including the new underground in Mumbai, bullet trains, the network of major highways connecting cities and the rapid increased acceptance of on-line payments. It is clear that India is on a journey to modernization at breakneck speed.

The country has emerged as a global hub for technology, manufacturing and services with major companies moving operations into the country. “Apple Aims to move half its supply chain from China to India where a quarter of the world’s iphones will be made” (Wall Street Journal). “Boeing’s deal with Air India is the biggest in civil aviation history” (CNBC);=. “Amazon will invest $12.9 billion in India by 2030 to build new data centers” (Nikkei Asia). And the list continues…

India is uncorrelated with major markets in the world – as reported by Bloomberg: 0.27 versus NASDAQ; 0.43 versus MSCI World Index; 0.49 versus FTSE and 0.33 versus S&P 500 and is a stock picker’s dream market with significant alpha potential especially in smaller companies outside of the Index. There is an abundance of quality companies that are not yet recognized by the market which offer huge growth opportunities vs. investment in companies that have already been publicly acknowledged and peaked. Indices are backward looking (reflecting successes already realized) and ignore smaller companies which have outperformed larger ones over the past decade due to their agility and ability to adapt quickly to changing market conditions.

However, investing in India is not without its hurdles. Issues such as regulatory complexity, political volatility, environmental degradation and social inequalities pose significant risks. Navigating the complex market structure requires more than just financial analysis – it requires a deep understanding of the Environmental, Social and Governance (ESG) factors that drive investment returns. The ability to accurately identify these factors and apply their impact on the future of a company is imperative to mitigate risk and enhance returns.

ESG Integration

ESG analysis cannot just be an add-on or an after-thought. It must be incorporated throughout all stages of the investment process in order to understand a company’s long-term financial return potential, structural growth drivers and their overall societal impact. This can be achieved through several approaches:

1) Negative Screening: Excluding companies or sectors that do not meet certain ESG criteria. For example, avoiding investments in companies with poor environmental records, unethical labor practices or those where revenues or profits are derived from areas that provide no environmental or societal benefits.

2) Positive Screening: Actively seeking companies that are making significant contributions to sustainable practices, social progress and ethical governance. This includes investing in firms with demonstrated environmental stewardship, social responsibility and robust governance practices.

3) Qualitative assessment: No two companies are alike, and external sustainability rating assessments may not provide sufficient in-depth analysis. Meeting with company management and discussing their approach to the environment, staff and minority shareholders can provide invaluable insights in identifying leaders.

4) Engagement: Engaging with companies to encourage better ESG practices. Investors can use their influence to promote improvements in corporate behaviour and policies. This is particularly important in a market such as India, where ESG investing remains in its infancy.

Furthermore, identifying key performance indicators that can be monitored on a continual basis is imperative to tracking the progress of a company and quantifying commitments and targets. These indicators represent a general set of transparency and ESG standards that firms are expected to meet over time.

Prioritizing ESG factors, as well as traditional financial analysis, enables investors to focus on the next story, not the last, and to thus identify new opportunities before they become mainstream and the broader market catches on.

Conclusion

As India continues its trajectory of economic growth and structural reforms, integrating ESG principles into investment strategies is not only a moral imperative, but can pave the way for long-term value creation and stakeholder prosperity. As global regulatory requirements become more closely aligned and mandated across investment platforms, partnering with skilled and experienced investment professionals is key to successfully meet your targets and ultimate goals.

Embracing sustainability is not just about doing good—it is about harnessing opportunities for growth, resilience and sustainable prosperity in India’s dynamic landscape.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

In the search for opportunities that can provide additional financial returns, investors often incorporate considerations beyond traditional financial metrics into their investment decision-making process. This concept is known as return additionality. The circular economy, where materials and resources are reused and waste is avoided, can potentially offer economic benefits and may be an avenue for return additionality.

A study by Oxford University revealed that companies with robust Environmental, Social and Governance (ESG) practices often experience lower risk and greater long-term financial performance. This same study stated that companies which have specific and effective ESG strategies achieve better operational performance, and their stock price performance is positively influenced by good sustainability practices .

This may provide an opportunity for investors to identify companies that might have unrealized opportunities for revenue growth or expense savings and to encourage them to adopt circular economy practices across their operations. This shift is not just theoretical; it is already happening. Between January and September 2020, public equity fund assets focused on the circular economy increased sixfold, from US $0.3 billion to US $2 billion, according to the Ellen MacArthur Foundation.

Benefits to companies and investors

1. Saving on packaging costs

In our economy, we can see wasted resources in countless industries and situations. Packaging, for instance, can constitute a good portion of the overall cost of goods sold. Most of this value is lost once the consumer discards the package. To recuperate this value, the market is currently concentrating on recycling materials like plastic to create new products, such as outdoor furniture, construction materials and yoga mats. However, only a small portion of these recyclable material inputs are being reused (less than 12% in the EU, for example).

Reusing packaging at a larger scale may represent a potentially significant opportunity. The beauty industry, for example, tries to reduce packaging costs by using bigger bottles. Certain restaurants and grocery stores in the U.S. offer discounts to consumers who bring reusable containers: the Just Salad restaurant chain offers free toppings for customers with reusable containers . Several major hotel chains (Mariott International, Hyatt Hotels and InterContinental Hotels) are replacing single-use shampoo bottles with re-fillable ones.

Consumers are increasingly prioritizing sustainability. According to a study from Nasdaq, Gen Z shoppers worldwide are willing to pay up to 10% more for a sustainable product . They are more interested in sustainability-related concerns than the brand names themselves and they place value on sustainability over cost saving measures. As consumer preferences shift towards sustainable products and services, companies that consider sustainability are better able to build customer loyalty, capture market share and drive revenue growth. Also, innovative waste reduction programs and sustainable product designs can boost a company’s brand and public profile, better positioning it in the green economy.

3. Boosting supply chain resilience

The current linear economic model can lead to resources scarcity and eventually depletion, but a circular model can help to mitigate supply chain risks. By using fewer raw materials, companies are less exposed to the price volatility of these materials. This stability can assist with the decrease of the cost of goods sold while helping with long-term planning as it reduces the dependance on new raw material integration.

4. Managing emissions

Reducing greenhouse gas (GHG) emissions is a core pillar of the circular economy. To achieve net-zero by 2050, our economy would benefit from the redesign of products, such that they are made with reusable resources. By reducing waste at multiple stages (from production to disposal), companies can reduce the need for production, thereby cutting emissions. Waste reduction also brings down the amount of material in landfills, which decreases methane emissions. With net-zero commitments for 2030 and 2050 becoming the norm, companies have an opportunity to innovate and implement best practices to reduce cost while meeting net-zero commitments (as opposed to buying carbon offsetting credits, for example).

5. Anticipating future regulations

Regulations related to the circular economy are expected to expand rapidly worldwide. For example, the European Commission adopted an action plan for a circular economy in 2019. In 2022, heads of state and global government representatives committed to developing by the end of 2024 an international legally binding agreement to end plastic pollution. The circular economy is also a key pillar of the European Green Deal, a set of policies approved in 2020 which aim to make the bloc carbon-neutral by 2050. Countries outside of the E.U., such as Chile and China, have already adopted ESG-related regulations aimed at promoting a circular economy. By cultivating an innovative and forward-thinking mindset, companies can start to implement circular economy policies and procedures. This can help them avoid potential future fines, reduce cost and risk, and leverage first-to-market brand opportunities.

6. Diversifying operations

Participating in the circular economy can help to diversify a company’s operations when it comes to the design and production of products. This is because in the circular eco-system, companies use old materials to create new things and design products with longer lifespans. This value recovery can be further developed and implemented at scale for greater economic gain.

Conclusion

The circular economy is often seen from a GHG emission reduction perspective, but it can also offer economic benefits. Shareholders can leverage these benefits when looking for growth investment opportunities or opportunities for existing investee companies to reduce expenses. Implementing a circular economy model can help companies achieve financial savings by recapturing wasted value. As investors continue to look for return additionality, they can encourage companies to implement circular economy practices, which could improve financial returns while contributing to positive environmental changes.

Contributor Disclaimer

The information contained herein is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

This material is not an offer to any person in any jurisdiction where unlawful or unauthorized. These materials have not been reviewed by and are not registered with any securities or other regulatory authority in jurisdictions where we operate. Any general discussion or opinions contained within these materials regarding securities or market conditions represent our view or the view of the source cited. Unless otherwise indicated, such view is as of the date noted and is subject to change. Information about the portfolio holdings, asset allocation or diversification is historical and is subject to change.

This document may contain forward-looking statements (“FLS”). FLS reflect current expectations and projections about future events and/or outcomes based on data currently available. Such expectations and projections may be incorrect in the future as events which were not anticipated or considered in their formulation may occur and lead to results that differ materially from those expressed or implied. FLS are not guarantees of future performance and reliance on FLS should be avoided.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank. ® The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

As the landscape of responsible investment (RI) continues to evolve, the theme of “Rising to the Challenge” encapsulated the industry’s unwavering commitment to progress despite unprecedented obstacles. At the 2024 RIA Conference, industry leaders and professionals gathered to address the pressing challenges and explore innovative solutions that drive sustainability forward. From regulatory shifts to geopolitical tensions, the responsible investment community demonstrated resilience and adaptability, reaffirming its dedication to fostering positive change and sustainable growth in an ever-changing world. The conference also highlighted the proactive measures and strategic insights necessary to navigate these complexities, ensuring that responsible investment remains a powerful force for good.

Held in Vancouver in May, the RIA Conference brought together over 300 responsible investment professionals from across Canada to explore the latest trends, challenges, and opportunities for the industry. Structured around several key themes, the 2024 Conference provided attendees with deep insights into sustainability practices, regulatory developments, and the future of responsible investment.

Navigating Regulatory Developments

A significant portion of the Conference was dedicated to understanding and anticipating regulatory changes. The ‘2024 Regulatory Roundtable’ session provided a comprehensive overview of proposed and current regulations around sustainability disclosures impacting the RI industry. Discussions covering topics critical to both advisors and investors, including the proposed CSA standards and disclosure rules; the duty of advisors and due diligence obligations; and fund labelling and global regulatory frameworks.

Global Challenges and Perspectives

A key session, ‘Responsible Investment in a Time of Populism’ explored the rise of populist movements and the geopolitical tensions that exacerbate uncertainties for responsible investors. The discussion delved into the latest polling data to illustrate how changing societal attitudes and dynamics could impact investment strategies, emphasizing the need for resilience and adaptability. Panelists shared actionable advice on mitigating portfolio risks and anticipating the potential repercussions of populist policies on global markets.

Keynote speakers also provided important perspectives on building a more sustainable and inclusive economic system and emphasized the role of RI principles in driving positive change and innovation. In his luncheon keynote, ‘RI in a Globalized Economy,’ Paul Clements-Hunt emphasized the important history of ESG principles, how they have evolved and the role of RI in driving positive change and innovation.

Furthermore, the conference tackled skepticism around ESG investing, including the challenges associated with ESG metrics, such as the perception of compromised financial returns and the contentious debate around the standardization of ESG criteria. Experts dispelled common myths and highlighted the importance of robust, transparent practices in fostering long-term sustainability and investor confidence.

Indigenous Rights and RI

Integrating Indigenous rights into RI practices was also significant theme at this year’s conference. The session ‘Integrating Indigenous Rights with ESG Principles’ underscored the importance of respecting Indigenous sovereignty, reconciliation and consent within investment frameworks, highlighting how such integration fosters meaningful relationships with Indigenous communities and enhances sustainable investment strategies. The focus on Indigenous rights emphasized a holistic approach to ESG, ensuring that investments contribute positively to social equity and long-term environmental stewardship.

Retail Advisors: Servicing the Client RI Gap

The opportunity for retail advisors to better service clients was thoroughly explored, focusing on the dynamics of advisor-client relationships and the role of wholesalers in promoting responsible investment. The session ‘Bridging the Client RI Gap: Innovative Practices for Advisors’ provided strategies to align client expectations with sustainable investment practices, while the discussion in ‘Driving Responsible Investment: Perspectives on the Wholesaler-Advisor Relationship’ highlighted the importance of open communication and collaboration. Together, these sessions underscored the critical role of retail advisors in advancing RI principles and enhancing client outcomes.

Transition to Net Zero

The journey to net zero was a central theme, emphasizing the crucial role of innovation and data integrity in achieving climate goals. Key sessions included:

Innovations, Developments, and Opportunities in Canada’s Energy Transition: Focused on advancements in renewable technologies, carbon capture and nuclear energy and highlighted the potential of these innovations to reduce carbon footprints.

Critical Minerals and Mining – Balancing Net-Zero Ambitions with Social Responsibilities: Discussed the need to balance economic opportunities with social and environmental responsibilities while recognizing Canada’s pivotal role in supplying minerals essential for the green economy.

Getting Accurate Sustainability Data: Addressed the challenges of current sustainability data, which is often estimated and unverified and advocated for more reliable and verified information to enhance investment decisions.

Climate Resilience – Managing Physical Risks in Your Portfolio: Explored strategies for adapting to and mitigating the impacts of climate change and stressed the importance of resilience in investment portfolios.

These sessions provided a comprehensive view of the path to net zero, combining technological innovation, responsible resource management and robust data practices.

Insights into Future Responsible Investment Practices

The conference concluded with a discussion on the future of RI, with insightful exchanges on evolving trends and strategic directions. The ‘Insights from Asset Owners’ session provided diverse perspectives on balancing beneficiary needs with emerging risks and opportunities, emphasizing the importance of sustainability in investment strategies. The concluding session, ‘Financial Markets as a Force for Good’, explored innovative approaches and emerging trends in harnessing finance to drive sustainable development and positive investment performance. Together, these discussions highlighted the potential of RI to build a more equitable and resilient global economy.

2025 RIA Conference Toronto

The 2024 RIA Conference was a resounding success, offering attendees a wealth of knowledge, practical strategies and opportunities for networking. The themes explored throughout the Conference underscored the importance of sustainability, regulatory awareness and innovative approaches to responsible investment. We look forward to continuing these vital conversations on June 3-4, 2025, at the 2025 RIA Conference in Toronto.

Five main drivers are responsible for biodiversity loss: climate change, pollution, overexploitation of natural resources, changes in land and sea use, and invasive non-native species. Many business activities contribute to these pressures, with the food, energy, infrastructure, and fashion value chains accounting for 90% of human-caused pressure on biodiversity.

What’s at stake

Biodiversity and ecosystems touch every aspect of human life. From the food we eat to the medicine we need, humans are heavily reliant on functioning ecosystems. More than 75% of global food crops rely on animal pollination, and over 70% of medicines used to treat cancer are natural or synthetic products made possible because of biodiversity.

Given these dependencies, biodiversity loss can translate into a wide range of risks for companies, including risks to operations resulting from supply chain disruptions, liability risk, price volatility risk, and regulatory, reputational and market risks.

Additionally, ecosystem loss has major implications for tackling the climate crisis. Land and the oceans absorb more than half of all carbon emissions produced by human activities, but as ecosystems disappear, nature’s ability to act as a “carbon sink” will be diminished and the consequences for our fight against climate change could be severe. Emissions reductions must therefore be coupled with measures to protect biodiversity if we are to meet our net-zero goals.

Regulators and investors take action

Since the Kunming-Montreal Global Biodiversity Framework was adopted in 2022, biodiversity – and nature more broadly – has been moving up the agenda for investors and regulators.

Key players are taking real action against the global threat of biodiversity loss, and we expect to see a continued focus on this issue. Numerous regulatory measures have been put in place, including the EU Deforestation Act, the EU’s Corporate Sustainability Reporting Directive, and Article 29 in France, all of which require increased company disclosure on impacts and dependencies on nature.

Investors are increasingly examining the financial risks associated with biodiversity loss. The Taskforce for Nature-Related Financial Disclosures (TNFD) launched their final framework to evaluate these financial risks in September 2023. The TNFD guidance is closely aligned to the Task Force on Climate-Related Financial Disclosures framework, incorporating the same four pillars of Governance, Strategy, Risk Management, and Metrics & Targets. The TNFD framework provides an essential starting point for companies to begin identifying, assessing, and disclosing their nature-related impacts and dependencies.

Other investor-driven engagement initiatives such as the Finance for Biodiversity Foundation, Nature Action 100, and the PRI Stewardship Initiative on Nature are beginning to take shape and gain momentum.

As companies realize that continued access to capital is increasingly contingent on making meaningful progress towards true stewardship of nature, real change with generational impact will follow.

Vancity Investment Management Ltd. is the sub-advisor of the IA Clarington Inhance SRI Funds.

iA Clarington Investments Disclaimer

For definitions of technical terms in this piece, please visit iaclarington.com/glossary and speak with your investment advisor.

The information provided should not be acted upon without obtaining legal, tax, and investment advice from a licensed professional. Statements by the portfolio manager or sub-advisor represent their professional opinion and do not necessarily reflect the views of iA Clarington. Specific securities discussed are for illustrative purposes only and should not be considered a recommendation to buy or sell. Mutual funds may purchase and sell securities at any time and securities held by a fund may increase or decrease in value. Past investment performance may not be repeated. Unless otherwise stated, the source for information provided is the portfolio manager. Statements that pertain to the future represent the portfolio manager’s current view regarding future events. Actual future events may differ.

Commissions, trailing commissions, management fees, brokerage fees and expenses all may be associated with mutual fund investments, including investments in exchange-traded series of mutual funds. The information presented herein may not encompass all risks associated with mutual funds. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. Trademarks displayed herein that are not owned by Industrial Alliance Insurance and Financial Services Inc. are the property of and trademarked by the corresponding company and are used for illustrative purposes only.

The iA Clarington Funds are managed by IA Clarington Investments Inc. iA Clarington and the iA Clarington logo, iA Wealth and the iA Wealth logo, and iA Global Asset Management and the iA Global Asset Management logo are trademarks of Industrial Alliance Insurance and Financial Services Inc. and are used under license. iA Global Asset Management Inc. (iAGAM) is a subsidiary of Industrial Alliance Investment Management Inc. (iAIM).

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

According to Bloomberg Intelligence, Global Environmental, Social, and Governance (ESG) assets are predicted to hit $40 trillion by 2030, despite macro challenges. Among the methodologies utilized, two common strategies that exist today are known as: ESG exclusion, the intentional exclusion of certain sectors or companies, and ESG integration, the integration of ESG factors into one’s fundamental analysis.

The Efficacy of Exclusion

The exclusionary approach was one of the first iterations of ESG investing, resulting in the divestment from companies in sectors deemed “bad” or “brown,” excluding them from investment portfolios. Sectors commonly subjected to exclusion include weaponry, tobacco, coal, nuclear energy, and oil and gas.

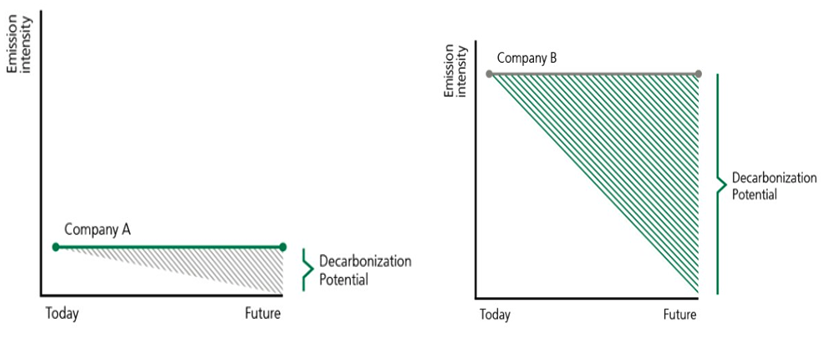

While the exclusionary approach can avoid exposure to these “bad” or “brown” sectors, studies have shown the long-term ineffectiveness in this approach. In a recent paper, Kelly Shue of Yale’s School Of Management and Samuel Hartzmark of the Carroll School of Management at Boston College, concluded “investing that directs capital away from brown firms and toward green firms may be counterproductive in that it makes brown firms more brown without making green firms more green”. When a heavily polluting firm is starved of capital, they are most likely to revert to the cheapest (and often most polluting) methods of production to continue to generate cash. If that same “brown” company wanted to improve their practices, while facing divestment, the firm would not have the capital required to make the investments and changes needed while conducting business as usual. Shue and Hartzmark also observed that a heavily polluting “brown” firm that reduced its emissions by just 1% would have a much greater impact than a typical “green” firm that reduced its emissions by 100%. See Figure 1 which highlights the decarbonation opportunity of a high emission intensity company.

Figure 1: Low emission intensity company (Company A) vs. a high emission intensity company (Company B)

Unlike an exclusionary approach, ESG integration does not limit the investable universe. Rather, it incorporates the consideration of ESG risks and opportunities into fundamental analysis.

A 2022 study by Capital Group found that 60% of investors cited ESG integration as the ESG approach most used. At Waratah Capital Advisors, we look for opportunities in “ESG improvers” that show positive ESG momentum through our ESG integration strategy that we have run since 2018. Consider a company with a historical reputation for poor ESG practices that is also behind its peers in implementing ESG considerations. The company would be deemed an ESG improver if it began demonstrating tangible ESG improvements. By providing capital to firms considered ESG improvers, we can help to “make the bad better” and be more impactful long term.

An example of a potential ESG improver is Canadian Natural Resources (“CNQ”). CNQ is one of the largest independent crude oil and natural gas producers in the world. Despite oil and gas companies often being in the spotlight for their negative environmental impact, they possess the ability to drive meaningful, positive advancements toward the world’s Net Zero target which is crucial in meeting the Paris Agreement. The International Energy Agency (IEA) has deemed carbon capture, utilization, and sequestration as an essential technology in their Net Zero by 2050 Roadmap. CNQ is currently the largest owner of carbon capture capacity in the Canadian crude oil and natural gas sector. Holistically, we believe their overall ESG practices are among the top of their peer group. We see CNQ in a position to lead peers as an ESG improver, not only in the net zero transition but also in industry ESG best practices.

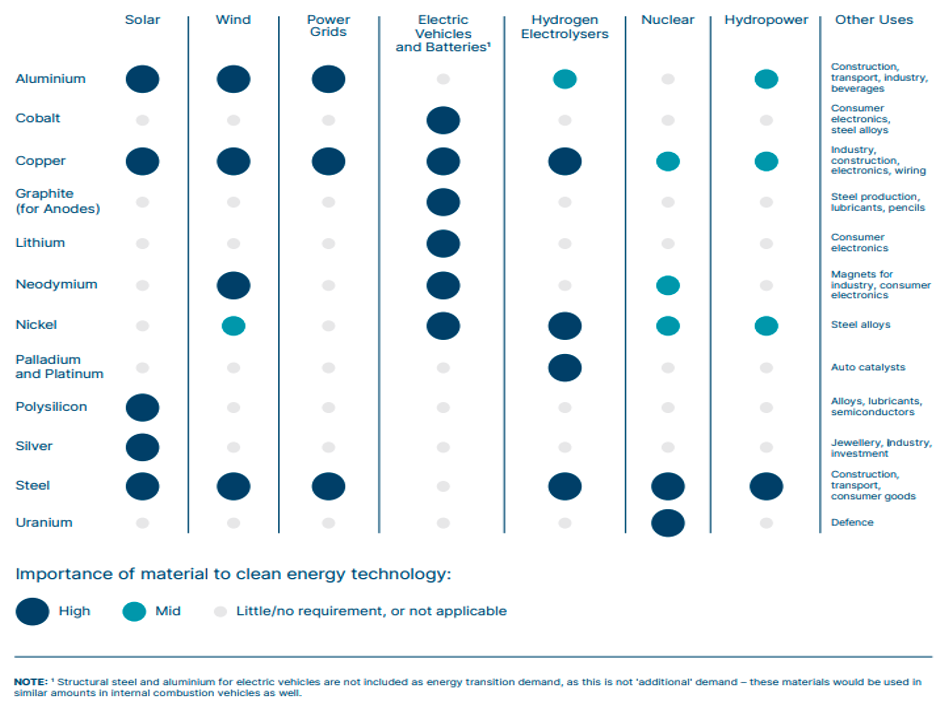

Companies within the mining sector have historically been viewed as negative ESG actors, due to the high environmental and social risks. The IEA deems several critical minerals, such as copper, lithium, nickel, and cobalt, as having an imperative role in the net zero transition. Mining companies, with exposure to energy transition minerals, will be essential to successfully build clean energy technologies. As shown in Figure 2, copper is of high importance to solar, wind, power grids, electric vehicles and batteries, and hydrogen electrolyzers as well as being of mild importance to nuclear and hydropower technologies. ESG improvers in this space show real signs of change, working on initiatives towards reducing emissions, improving operational efficiency, and demonstrating positive progress in their ESG performance data.

Figure 2: Materials used in clean energy technology

By solely divesting from a “brown” or “bad” ESG company, investors lose out on the opportunity to invest in change. ESG integration strategies allow investors to dig deeper into a company’s practices, compared to just looking at them from the surface through an exclusionary approach. Investors can put a spotlight on the “bad” ESG companies that are showing real signs of positive ESG momentum and in turn, have more opportunity and impact to make a change across all sectors.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Canadians are obligated to respect human rights in Canada and around the world. In this article we raise awareness regarding elevated human rights risks to Indigenous Peoples in Latin America and what investors can do to fulfill their human rights due diligence responsibilities across all regions under evolving regulatory and stakeholder expectations.

Demand for minerals to support the energy transition is anticipated to soar over the next years and decades. Indigenous Peoples around the world are at risk of being disproportionately impacted despite contributing the least to climate change given 50% of known transition minerals are located on or near to their traditional lands. These Peoples also protect and maintain up to 80% of the world’s remaining biodiversity. While Canadian institutional investors are increasingly aware of and educated on how to respect Indigenous rights and reconciliation in the Canadian context, there is less awareness of best practices to ensure respect for Indigenous Peoples’ rights in other regions and contexts. At the same time, investors are increasingly expected to account for adverse impacts on people and planet linked to investing and financing activities under voluntary standards like the United Nations Guiding Principles for Business and Human Rights (UNGPs) and new related mandatory sustainability laws like the European Union’s Corporate Sustainability Reporting Directive (CSRD). Major Canadian financial institutions and other large Canadian corporate entities with European subsidiaries or branches and a certain amount of turnover in the European Union, may eventually have to report against them. Given the extent of Canadian mining activities in Latin America, we outline significant risks to Indigenous rights from land-based projects in that region and what investors can do to help prevent and mitigate related human rights and investment risks.

The Human Rights Context of Indigenous Peoples in Latin America

Canadian companies in scope of the European Union’s mandatory CSRD will be required to disclose the most material impacts on society and the environment from business activities and how these are being managed as implementation of the law expands over the next few years. Evidence finds that severe impacts on human rights related to resource development occur most frequently in Latin America and disproportionately impact Indigenous Peoples.

Threats include multiple cumulative negative impacts from business and industrial activities, criminal groups and the compounded effects of climate change and environmental degradation that infringe on rights to safety and security, and the right to enjoy traditional cultural practices and livelihoods, amongst other human rights. Many Indigenous leaders have been persecuted, targeted, and even assassinated for defending their rights in these contexts.

Latin America is also home to an estimated 185 distinct Indigenous populations in voluntary isolation, whose rights to remain isolated are enshrined in international laws such as the Universal Declaration of Human Rights and the United Nations Declaration on the Rights of Indigenous Peoples.

While the concept of economic reconciliation as a benefit of resource development has gained traction in the context of negotiations with Indigenous governments in Canadian, it may be foreign to many Indigenous Peoples in Latin America, and it cannot necessarily be assumed that such concepts are welcomed in all sectors. This underscores the importance of a rights-based approach in every context that centres around the need for proponents to seek out and respect local perspectives through good faith due diligence, avoid complicity, and respect for the right to free prior and informed consent (FPIC).

Environmental and Climate Risks

Latin America is home to many unique ecosystems and habitats, including the Amazon, that are critical for ensuring the livelihoods of its inhabitants including Indigenous Peoples and for global climate change mitigation and biodiversity protection. Respect for, and protection of Indigenous Peoples rights, including to their lands, resources and territories is proven by research as necessary for protecting nature.

Indigenous Peoples’ organizations have been clear about the need to reverse the trend towards irreversible tipping points. The Coordinator of Indigenous Organizations of the Amazon River Basin (COICA), along with other organizations have called for the protection of 80% of the Amazon by 2025, strict adherence to free, prior and informed consent, a moratorium on deforestation and degradation of primary forests, among other interventions.

Canadian Company Involvement in Latin America

Canada, being home to many companies in the mining sector, also hosts a significant share of the mining companies operating in Latin America. 2014 estimates were that between 50 – 70% of mining activity in Latin America involves Canadian mining companies. The same report found that the lack of consultation and implementation of FPIC by Canadian mining companies in Latin America was the rule rather than exception. Other reports have found many examples of Canadian companies with operations in Latin America being linked to acts of violence. In 2023, a coalition of more than 50 civil society organizations published the report “Unmasking Canada: Rights Violations Across Latin America,” highlighting human rights issues connected to 37 Canadian projects across Latin America and the Caribbean.

The Legal Context of Indigenous Peoples’ Rights and Associated Obligations in Latin America

While articulated most clearly through the UN Declaration on the Rights of Indigenous Peoples, Indigenous Peoples’ rights in Latin America are also protected by various legal frameworks and instruments*, national constitutions, national legislation, and judicial decisions.

For example, the Inter-American Court of Human Rights has established that the State must abide by the following safeguards: effective participation (including FPIC), reasonable sharing of benefits from any development plans within the territory, and that no concessions on Indigenous territory are granted before prior environmental and social impact assessments are conducted.

Many national court rulings have also established safeguards that in effect, require FPIC. For example, in Colombia and Brazil, courts have ruled that Indigenous Peoples’ own autonomous free, prior and informed consultation and consent protocols and laws are binding.

However, those rights and obligations are in practice only implemented after investments have been made, leading to significant risks. For example, in Ecuador, a decree regulating permitting with affected Indigenous Peoples was later ruled to be unconstitutional and suspended by Ecuador’s constitutional court for failing to guarantee the constitutionally enshrined rights of Indigenous Peoples in Ecuador, thus generating significant risks for mining projects. In Peru, a regional court found that the granting of concessions to businesses on Indigenous territories where formal Indigenous land title had not yet been granted was unlawful. It is this gap between international and, or constitutionally enshrined Indigenous rights and lack of protection of these rights by local and regional authorities that presents significant risks for both adverse human rights impacts and investments.

Priority Investor Actions

Institutional investors in Canadian mining companies can help ensure investee companies ‘mind the risk gap’ by advocating for them to adopt and implement, in every case, rights-based approaches that align with international human rights standards regardless of whether local and regional authorities actively respect and protect these rights. The UNGPs were developed over a decade ago to explicitly address this risk gap and ensure multinational companies operating abroad respect human rights no matter where they operate. They now provide the foundation upon which mandatory corporate sustainability laws, like the CSRD, and France, Germany, and other EU member states’ supply chain due diligence laws, are based. While investors can advocate for benefit-sharing mechanisms and other types of partnerships that create more equitable economic and social benefits from mining or other resource development activities on the traditional territories of Indigenous Peoples, the starting point should be a rights-based approach, including FPIC giving due consideration to the local legal and human rights context, and risks to Indigenous human rights defenders.

Key immediate actions Canadian investors can take to add to their due diligence include:

– Screen all portfolios for company involvement in Latin America, with a focus on land and resource-intensive sectors and conduct enhanced due diligence to understand implications for locally affected Indigenous Peoples;

– Ask investee companies for disclosures of evidence of FPIC;

– Consult Indigenous Peoples’ representative institutions or others from civil society working with Indigenous Peoples in Latin America regarding appropriate investor action;

– Spread awareness of the need for urgent investor action on human rights in Latin America

Contributor Disclaimer

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties, and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate. Certain of the products and services offered under the brand name, BMO Global Asset Management, are designed specifically for various categories of investors in Canada and may not be available to all investors. Products and services are only offered to investors in Canada in accordance with applicable laws and regulatory requirements.

®/™Registered trademarks/trademark of Bank of Montreal, used under licence.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.

Pressure mounts to rethink balance sheets to account for natural capital—arguably the world’s most important asset. Are you prepared?

Nature is deteriorating at an alarming rate, and with over half of the world’s GDP (US$44 trillion) at risk due to rapid biodiversity loss, environmental degradation is quickly climbing to the top of corporate and investor agendas.

In a major step forward, the international Taskforce on Nature-related Financial Disclosures (TNFD) released landmark guidance last September to help organizations identify and assess nature-related risks, impacts and dependencies. Interested and affected parties in many jurisdictions, including Canada, are evaluating the standards and international developments to determine the best path forward.

Having finalized its climate and general requirements standards in June 2023, the International Sustainability Standards Board (ISSB), an independent standard-setting body charged with streamlining sustainability reporting by developing a global baseline, has turned its attention to discerning its next areas of focus. In April 2024, the ISSB announced that it will commence a research project on the disclosure of risks and opportunities associated with biodiversity, ecosystems and ecosystem services, shining a spotlight on the value of accounting for nature.

Following the release of the TNFD’s risk management and disclosure framework, the ISSB announced that it would “look to the TNFD recommendations—where it relates to meeting the information needs of investors—in its future work.”

Improving nature-related practices and disclosures

A growing global network of TNFD consultation groups is working diligently to identify knowledge gaps on nature-related issues and to engage with regional markets on its recommendations. The Chartered Professional Accountants of Canada (CPA Canada) and the Institute for Sustainable Finance (ISF), as co-convenors of the Canadian consultation group, are responsible for fostering awareness, education and capacity building for TNFD in Canada.

For more than 20 years, the Canadian accounting profession has been at the forefront of championing sustainability as a good business practice. With a long history of ensuring that organizations manage risk and report credible information in the capital markets, the accounting profession will play a pivotal role in guiding organizations and investors through the integration of nature into decision making, helping turn ambitious environmental pledges into practical actions.

In resource-based economies like Canada, there is particular urgency to see stakeholders across the financial and corporate systems work collaboratively to shift business models, budgets and financial flows away from nature-negative to nature-positive outcomes. Investors increasingly recognize that they hold nature-related risk in their portfolios and want to understand how those threats are being managed to deliver robust financial returns and minimize environmental disruption. In fact, a 2023 study of ESG sentiment among institutional investors found that 63 per cent of respondents consider nature-related factors when making decisions.

Credible and comparable data is essential for building trust to drive effective capital reallocation and to attract new investments for scaling up sustainability efforts. The TNFD’s emphasis on transparency and accountability will help bridge the gap between financial markets and the natural world.

Climate and nature goals inherently linked

A collaborative and proactive approach to reporting could not be more urgent as climate change proves to be an increasingly important driver of biodiversity loss. Consequences of the climate crisis, from deforestation to water scarcity, can materialize as financial risks to businesses that inevitably impact the broader financial system. Conversely, restored ecosystems rich in biodiversity can enhance business operations, create new markets and play a critical role in achieving net-zero goals by removing carbon from the atmosphere.

Indigenous communities hold a profound connection to the land, rooted in centuries of stewardship and traditional knowledge. Despite comprising only 6.2 per cent of the world’s population, Indigenous Peoples safeguard an astonishing 80 per cent of the planet’s biodiversity, making the Indigenous perspective another vital component in combatting climate change and environmental degradation.

Natural capital underpins healthy societies and resilient economies. Halting and reversing nature loss hinges on our ability—as businesses, financial institutions and asset managers—to understand our dependencies and impacts on the natural world.

There is a significant need to empower both the users and preparers of climate- and nature-related information with best practices for disclosing sustainability performance. I can say with confidence that the CPA profession is up to the capacity-building challenge, but we are only one piece of the puzzle. With growing recognition of the intrinsic value of nature, investors are increasingly being called upon to finance this change.

Your blueprint for action

By aligning investment decisions with sustainability goals and advocating for robust reporting standards, investors are well positioned to drive transformation in nature-related reporting practices. Your role extends beyond mere financial support; your requests for transparency, accountability and standardized metrics have the power to catalyze a more holistic approach to accounting and reporting practices.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.