The 2025 RIA Investor Opinion Survey paints a nuanced picture of Canadian retail investors’ attitudes toward responsible investment (RI). While interest in RI remains strong and is even growing among certain groups, significant challenges around awareness, advisor engagement and concerns about greenwashing continue to temper enthusiasm.

According to the survey, two-thirds of Canadian investors express interest in responsible investing, with younger investors and women showing the highest levels of interest. Interestingly, the survey also notes a rising interest among those aged 55 and older, suggesting that RI is becoming a priority across generations. Despite this widespread interest, knowledge about responsible investment remains limited. About two-thirds of respondents admit to knowing little or nothing about RI, and nearly one in five have never even heard of the concept.

The influence of global events is also shaping investor behavior. Over a third of respondents say they are more likely to choose responsible investments now than they were a year ago. However, this increased interest has not yet translated into higher ownership, as RI holdings have slightly decreased since late 2023. This disconnect points to barriers beyond mere interest, including a critical gap in communication between investors and their financial advisors.

RI Service Gap

Source: 2025 RIA Investor Opinion Survey

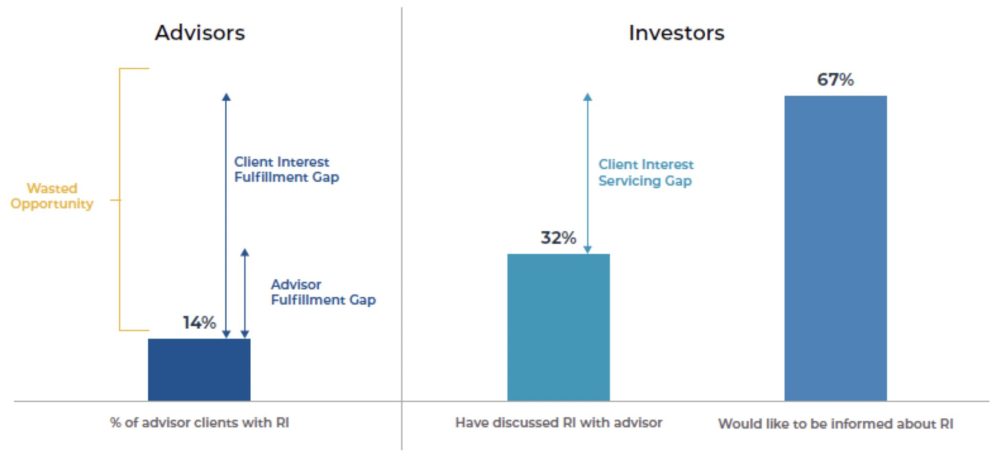

While a striking 76% of investors want their advisors or financial institutions to ask them specific questions about RI, only 28% report ever being asked such questions. Even when these conversations do occur, just 35% describe them as meaningful. This lack of engagement suggests missed opportunities for advisors to connect with clients and guide them toward investment choices that reflect their ethical priorities.

Greenwashing, the practice of marketing investments as more sustainable than they truly are, is once again a primary concern for investors. Despite the Canadian Securities Administrators (CSA) updated guidance on disclosures related to ESG considerations in March 2024, more than half of respondents now cite greenwashing as a deterrent to responsible investing, up from 46% previously. This increasing skepticism underscores the need for greater transparency and accountability in the RI space.

Artificial intelligence (AI) is another emerging area of interest and concern. Most investors are unfamiliar with how AI is applied in investment decision-making, with 64% reporting low or no familiarity. Yet, a majority believe it is important for companies in their portfolios, as well as their financial advisors and institutions, to adopt responsible AI frameworks and principles.

Ultimately, the survey reveals that Canadian retail investors value responsible investment not only for its potential to generate returns but also for its role in risk reduction and alignment with personal values. Nearly all respondents emphasized the importance of considering investment opportunities that incorporate RI in portfolios, and that financial advisors remain a trusted source of information for these decisions.

The 2025 RIA Investor Opinion Survey makes it clear that while interest in responsible investing is high and expanding, there is a pressing need for better education, more proactive advisor engagement, and stronger safeguards against greenwashing. Addressing these challenges will be key to turning investor interest into meaningful action and fostering a more sustainable investment landscape in Canada.

Responsible Investment Research Initiative

This report was produced as part of the Responsible Investment (RI) Research Initiative. A program of the RIA, the Initiative delivers objective, data-driven insights that give clarity on where the Canadian marketplace stands. The initiative is grounded in three marquee reports, published annually, providing a 360-degree view of responsible investment in Canada:

The Investor Opinion Survey (Learn more) brings the voice of everyday Canadians into the conversation. It tells us what retail investors think, what they value and where responsible investment fits into their financial goals.

The Advisor RI Insights Study (Coming October 2025) explores how Canadian financial advisors approach responsible investing, including what they’re hearing from clients, what they’re recommending and where the barriers still lie.

The Canadian RI Trends Report (Coming November 2025) tracks the practices of institutional investors, from pension plans to fund managers, and helps us understand how responsible investment is evolving across Canada’s capital markets.

These reports speak to different segments of our ecosystem, but together they tell a powerful story of where we are, what we’re facing, and where we can go next. This initiative is about giving our members, and the broader investment community, the insights needed to set strategy, communicate with stakeholders, and measure progress.

The RI Research Initiative is generously supported by partners Addenda Capital, Desjardins, Mackenzie Investments, National Bank Investments, RBC Global Asset Management, and TD Asset Management. Learn more at www.ri-research-initiative.ca.