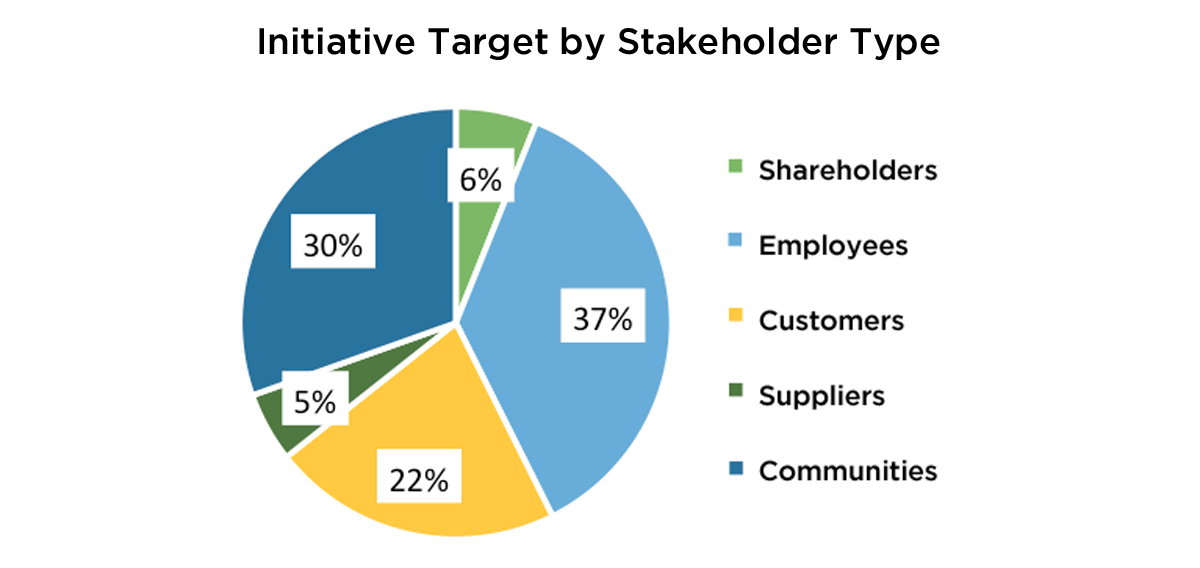

As long-time investors in catastrophe bonds (cat bonds) and insurance-linked securities (ILS) portfolios, we are seeing by their nature how these specialized investments can help actively promote environmental, social and governance (ESG) considerations.

ILS are used by insurers and reinsurers as an economically attractive alternative to traditional reinsurance. With these instruments, investors put up collateral through the securitization and share in a portion of reinsurance risk in exchange for the opportunity to earn premium income.

Cat bonds are a specific segment of ILS structured as floating rate 144A bonds to transfer reinsurance risk associated with natural peril events that are remotely occurring but highly costly for insurance markets. These uncorrelated and diversifying investments further support the potential capital required of re/insurers to cover losses so that rebuilding can occur for those impacted.

We believe there are a variety of key investment factors to consider in cat bonds/ILS that speak to an ESG mindset and the asset class can inherently promote ESG.

The cat bond/ILS market is a climate risk price indicator and can serve as a market-enforcement mechanism that encourages better climate risk management.

Large ILS constituents can play a role in how re/insurance addresses climate change impacts because trends such as rising temperatures and sea levels result in increased hazard frequency and severity created by hurricanes, tornados, winter storms, hail, and flooding. Insurance underwritten to help communities and economies deal with these events is priced according to risk level and modeling assumptions from weather and insured loss-based data. The greater the exposure level that a community or property seeking insurance has to these risks, the higher the premiums for their insurance will be, potentially impacting capital levels available to protect these communities.

If a community or property has taken steps to manage or mitigate these hazards – such as better structure engineering or placing buildings and structures in locations with sustainability-based development plans – they will be rewarded with lower premiums. Alternatively, if they have not pursued sustainable development strategies geared toward handling climate change impacts, they will be penalized with higher premiums.

The cat bond/ILS market promotes social and economic welfare.

Twenty-five years ago, global reinsurance firms were the only insurance providers that communities could rely on to address damages incurred beyond the amounts covered by their initial, primary insurance. Hurricanes Katrina and Harvey, as well Japan’s Tohoku earthquake, demonstrated the importance cat bonds/ILS can play in the insurance markets’ ecosystem by providing an additional funding source necessary to help people and communities rebound.

Cat bond/ILS market growth has enabled the creation of public insurance pools, whereby local government entities and sovereign nations – mostly in developing markets – can transfer re/insurance risks to capital markets.

Developing countries such as the Philippines and Columbia issue catastrophe bonds through the World Bank that enable them to get disaster recovery capital and mitigate the setbacks to growth and economic development that a catastrophic event could create. In the case of the Philippines , catastrophe bonds are helping to lessen typhoons’ impact on economic output.

Similarly, Mexico received a payout from a catastrophe bond issued by the World Bank after an earthquake in 2017. That money helped finance housing and public infrastructure reconstruction and rehabilitation in affected areas. Furthermore, several groups have formed a trust that purchased the first coral reef insurance policy to help support rebuilding coastal ecosystems following hurricanes’ or severe storms’ damage.

In the United States, state-run pools in Florida, Texas, and California, to name a few, have been issuing ILS for as long as 10 years to provide insurance to communities that couldn’t obtain it in private markets.

Many of the cat-bond/ILS instruments offer disaster-risk financing that is transparent and efficient.

One key ILS feature is the quick and efficient mechanism for issuing payouts once an event triggers insurance protection. These triggers are based on fully transparent measures, such as an events’ scale or losses exceeding a specific dollar amount. This design is deliberate and provides timely payouts in the wake of a disaster when money is most critically needed.

The World Bank has implemented these types of triggers successfully when partnering with developing nations to issue cat bond protection against impact from major hurricane, earthquake and pandemic-related events. In the current COVID-19 pandemic, two World Bank-sponsored bonds helped to provide financing to a handful of emerging markets in support of response efforts.

These mechanisms are a vast improvement over traditional governance of payments from private insurance markets, government, and non-governmental organizations, as those payments were not always issued in a sufficient and timely manner.

These securities are based on insurance designed to provide additional capital sources to aid the broader societal goal of helping countries and communities recover from disastrous events, thereby creating a category of investments with ESG goals as a foundational principle.

Overall, climate change, health funding, food supply issues and compromised infrastructure can all magnify the severity of economic losses suffered by communities and nations. The result can further widen the “protection gap” as economic losses suffered from major events such as hurricanes, droughts, and pandemics cannot be adequately covered by re/insurance capital alone.

Today, the presence of cat bond/ILS investors in this market helps provide critical capital influx to boost re/insurance capacity and increase the speed of access to capital. These beneficial results provide insurers with more flexibility to address protection gaps. Closing these protection gaps is a key component of insurers’ ability to build out more resilient ESG-oriented programs.

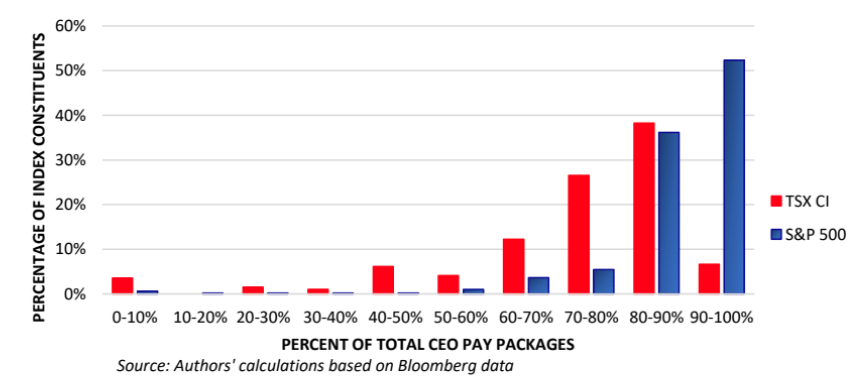

In reviewing executive compensation in 2019, NEI found base salaries in Canada did not exceed $2.5 million;[2] and in the U.S, they did not exceed US$5 million. And some CEOs, such as those at Facebook, Akamai Technologies Inc. and Prologis (all company founders) earned just one dollar in base salary.

In reviewing executive compensation in 2019, NEI found base salaries in Canada did not exceed $2.5 million;[2] and in the U.S, they did not exceed US$5 million. And some CEOs, such as those at Facebook, Akamai Technologies Inc. and Prologis (all company founders) earned just one dollar in base salary. As illustrated by the timeline, Shell engaged with shareholders throughout the process of establishing carbon goals and incorporating those goals into the executive incentive plans. Although some shareholder resolutions received relatively low support (~5%), they still put the pressure on Shell by emphasizing their focus on ESG.

As illustrated by the timeline, Shell engaged with shareholders throughout the process of establishing carbon goals and incorporating those goals into the executive incentive plans. Although some shareholder resolutions received relatively low support (~5%), they still put the pressure on Shell by emphasizing their focus on ESG.