The current lack of expertise in sustainable finance

Environmental, social and governance (ESG) considerations have become increasingly important for modern risk management and portfolio optimization. Governments, businesses and asset management firms are committed to achieving net-zero goals, and Canadians are showing more and more interest in responsible investment (RI). It is clear, however, that the financial services sector in Canada lacks advisors and investment experts with adequate knowledge of sustainable finance, and this is being felt by advisors and clients alike.

The figures speak for themselves

To examine this gap, Toronto Finance International (TFI) and Deloitte conducted research in 2021, which revealed the importance of developing skills and paved the way for inclusive sustainable finance expertise within organizations.

The study by TFI and Deloitte highlighted, among other things, the mismatch between supply and demand in financial institutions. In fact, 68% of respondents mentioned that there is a demand for sustainable finance skills but that the supply falls short.

The report also highlighted some recruitment and retention challenges, including how intensifying competition for ESG professionals and the growing need for specialized skill sets make it difficult to find and retain top talent.

This vicious cycle fueled by lack of expertise and talent in the sustainable finance space is being felt even by advisors, where the limited capacities of teams represent an obstacle to better training.

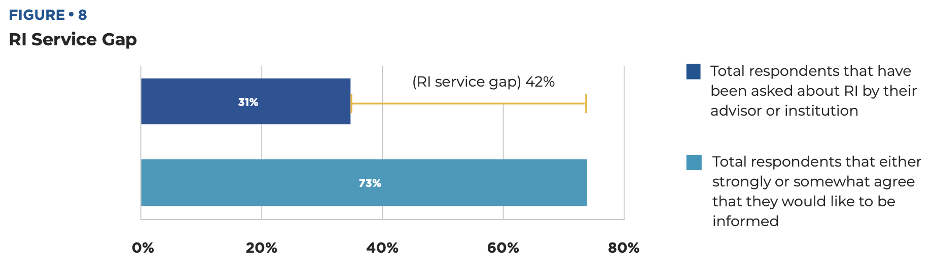

A persistent knowledge gap

Knowledge is essential for investment advisors since they are a conduit between investors and asset managers. Therefore, raising awareness and educating clients about responsible investment starts with educating advisors.

According to the Responsible Investment Association’s (RIA) survey of 1,000 retail investors, Canadians want to hear more about responsible investment, but 42% of investors who are interested in RI are not receiving information about it from advisors.

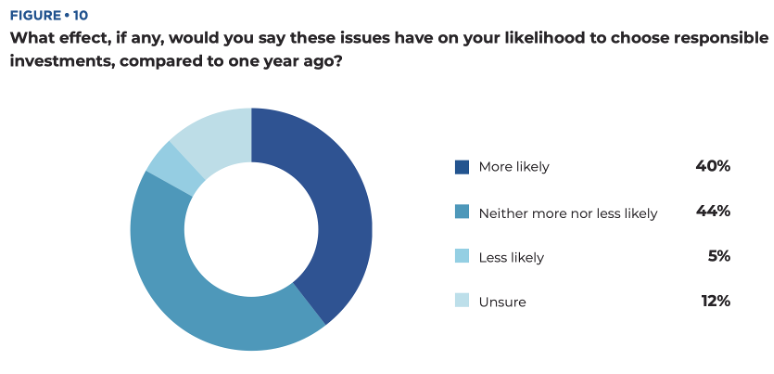

What are the risks for advisors and investors?

This service gap is not without consequences and can lead to undesirable situations.

Solutions not meeting clients’ needs

Another survey by the RIA found that advisors tend to overestimate their knowledge of responsible investment. An internal survey conducted at National Bank shows that they are aware of their own knowledge gap but are nevertheless interested and would like to improve their service offering with discussion about RI.

To ensure that the products are properly positioned, a good knowledge of the industry is required. Advisors must also be able to initiate discussion on responsible investment in order to fully understand the subtleties of their clients’ needs and to offer them appropriate solutions.

Clients may go elsewhere to have their needs met

Significant business opportunities can open up for advisors who are able to discuss RI preferences with their clients, inform them on the subject, and offer them solutions tailored to their needs.

Alternatively, clients who are dissatisfied with their advisor’s level of knowledge may seek expertise elsewhere.

What are some potential solutions?

As we have seen, the talent shortage is keeping knowledge from being transmitted and, consequently, training from being provided. There are, however, solutions to reduce this knowledge gap, for example:

Academic and professional training

An increasing number of RI organizations and associations, (RIA, PRI), universities, (John Molson School of Business, Queens) and professional groups (Finance Montréal, CFA, CSI) offer training programs to industry professionals seeking to deepen their understanding of responsible investment.

Education4sustainability has a tool that filters training provided by various organizations based on duration, price, and focus.

In addition, many organizations, including National Bank, have developed internal training courses focused on responsible investment for their employees. Some even provide such training to their clients.

Tools for greater transparency

To address the current confusion in the industry and make it easier for clients and advisors to understand, a few organizations such as the Canadian Securities Administrators are working to develop clearer frameworks. However, there is still work to be done to make content more accessible to all advisors and investors.

Support for advisors

Considering how quickly products, portfolio solutions and RI terminology are evolving, it’s difficult to provide in-depth, sustained, and relevant training to all advisors.

Advisors can always integrate questions relating to responsible investment into their KYC, and the market would do well to acquire digital solutions. Tools that support automated decision-making could be useful for advisors and would standardize questions specific to responsible investment. Such a tool would help advisors gain confidence and be better prepared to support clients.

Conclusion

The service gap resulting from the shortage of expertise in sustainable finance, among other things, is a complex problem that requires solutions on several fronts. However, by making it a priority to hire and retain skilled ESG professionals, by helping today’s workforce develop skills, and by providing tools to facilitate learning, the industry is making progress in closing this gap.

Contributor Disclaimer

The information and the data supplied in the present document, including those supplied by third parties, are considered accurate at the time of their printing and were obtained from sources which we considered reliable. We reserve the right to modify them without advance notice. This information and data are supplied as informative content only. No representation or guarantee, explicit or implicit, is made as for the exactness, the quality and the complete character of this information and these data. The opinions expressed are not to be construed as solicitation or offer to buy or sell shares mentioned herein and should not be considered as recommendations.

The information and opinions herein are provided for information purposes only and are subject to change without notice. The opinions are not intended as investment advice nor are they provided to promote any particular investments and should in no way form the basis for your investment decisions. National Bank Investments Inc. has taken the necessary measures to ensure the quality and accuracy of the information contained herein at the time of publication. It does not, however, guarantee that the information is accurate or complete, and this communication creates no legal or contractual obligation on the part of National Bank Investments Inc.

© 2023 National Bank Investments Inc. All rights reserved. Any reproduction, in whole or in part, is strictly prohibited without the prior written consent of National Bank Investments Inc.

® NATIONAL BANK INVESTMENTS is a registered trademark of National Bank of Canada, used under licence by National Bank Investments Inc.

National Bank Investments is a signatory of the United Nations-supported Principles for Responsible Investment, a member of Canada’s Responsible Investment Association, and a founding participant in the Climate Engagement Canada initiative.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.