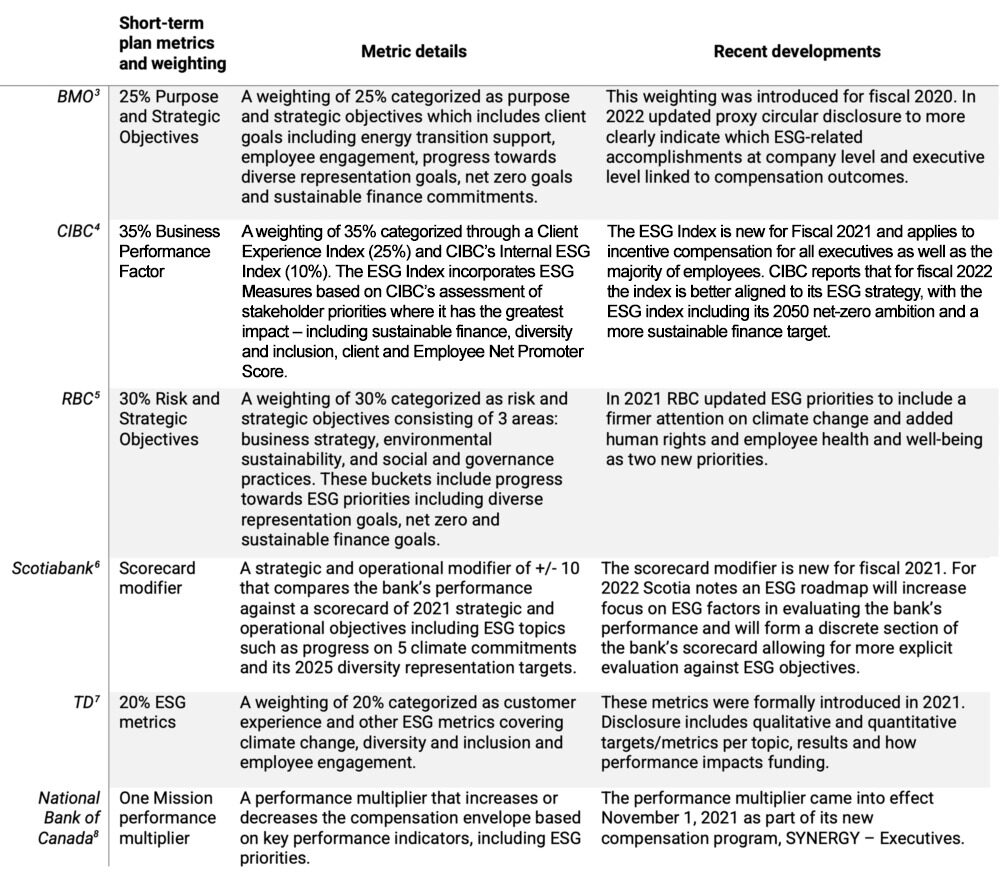

Amid the shifting global energy landscape and mounting investor pressure, many large publicly traded North American oil and gas companies have committed to achieving net-zero greenhouse gas emissions by 2050 in an effort to limit global warming to below two degrees Celsius.

With net-zero commitments come varying strategies on how each company will achieve these goals. Steep decarbonization in such a carbon-intensive industry requires significant capital allocation, and for some companies, a complete pivot away from fossil fuels toward renewables.

Climate supporters should rightfully cheer the commitments and transition efforts these companies are undertaking. However, these actions raise the question of what happens with carbon-intensive assets that still have a useful life, such as fossil fuel power stations, pipelines and wells, but which are not aligned with a company’s decarbonization plans. One approach is for firms to recoup value for shareholders and progress on their climate ambitions by selling these assets.

Trends in Oil and Gas Asset Transfers

A recent paper from the Environmental Defence Fund has shown that over the last five years, these assets are more often being acquired by companies whose climate commitments are lower or non-existent compared to the companies divesting of these assets[1]. Globally, between 2017 and 2021, 155 deals led to the transfer of assets from companies with a net-zero target to companies without a net-zero target. Similarly concerning, 211 deals moved assets from companies with a methane reduction goal to companies without methane goals.

Overall, 886 deals transferred assets from public companies to private companies, versus 541 from private companies to public companies. When an asset shifts from one public company to another public company, investors keep the ability to engage with the asset owner. However, when the asset shifts from a public company to a private operator, public equity investors lose that ability. Also, the private operator may not be subject to the same standard of reporting regulations and requirements as listed firms – and it may become more difficult to track the actual emissions from that asset or operator over time.

This in turn means that while the divesting company’s emissions may decrease with the sale of the asset, real-world emissions may stay the same, decrease, or in some cases even increase, depending on the purchasing company’s plans for the asset. Ultimately, this sale may negate any positive real-world climate impact.

Managed Phaseout

As fiduciaries, it’s imperative that asset managers stay up to date on best practices to manage risks and seize opportunities related to the low-carbon transition. The Glasgow Financial Alliance for Net Zero (GFANZ), a global coalition of leading financial institutions committed to accelerating the decarbonization of the economy, recently published The Managed Phaseout of High-emitting Assets, which provides a framework for companies to phase out carbon-intensive assets, rather than divest of them.

The managed phaseout approach is based on the view that certain high-emitting assets can continue to operate until a net-zero-aligned retirement date as an alternative approach to a pathway of steadily decreasing greenhouse gas emissions. This approach has the benefit of promoting an orderly transition and allows for financial institutions to remain engaged with companies in high-emitting industries.

Integrating Managed Phaseout and Responsible Asset Transfer into Engagement Strategies

As investors with a focus on managing climate risk, it is crucial that we prioritize the reduction of real-world emissions with issuers, as opposed to simply emissions transfers. This is something we should raise while engaging with companies which own carbon-intensive assets and are developing pathways for their net-zero targets. Key questions we can ask are: how big of a role will divesting play over the short to medium term to achieve interim targets? And do you evaluate prospective buyers on any environmental criteria?

Asset transfers are a normal part of company strategy and several factors go into any decision to divest of an asset. An offer must balance the legitimate need to maximize shareholder value with climate-related considerations.

On top of incorporating responsible asset transfer into engagement strategies, investors can encourage oil and gas companies to conduct scenario analysis and produce reports on the risk of assets in their business suffering from unexpected write-downs. It is crucial for companies to understand the risks and develop plans for a managed phaseout where responsible asset transfer may not be a viable option.

Looking Forward

As the net-zero transition continues, it is crucial for investors to remain supportive of oil and gas decarbonization efforts while prioritizing the reduction of real-world emissions. Investors can do so by encouraging investee companies to adopt responsible asset transfer policies and implement a framework for a managed phaseout of carbon-intensive assets.

Source:

[1] Copyright © 2022 Environmental Defense Fund. Used by permission. The original material is available at https://business.edf.org/insights/transferred-emissions-risks-in-oil-gas-ma-could-hamper-the-energy-transition/

Contributor Disclaimer

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.